July 10, 2023 •Nathan Willis

Key Events: A week without consensus

Economic data releases painted the picture of a slowing manufacturing sector, but a services sector that is showing momentum.[1]

Minutes from the Federal Reserve’s last meeting showed dissent among voting members as a few members favored another rate hike rather than the pause that occurred.

Market Review: Summer break

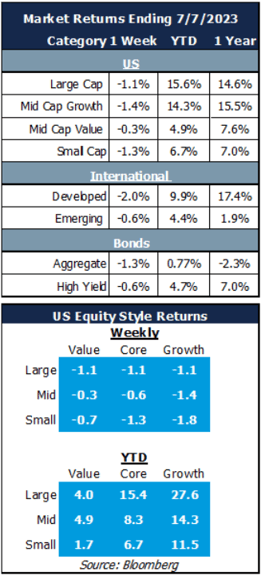

After a 16.9% return through the first half of the year, gains took a break. The third quarter began with a whimper as the S&P 500 dropped slightly; both small cap and international stocks joined in the declines.

Bonds lost ground as the market weighed the likelihood of further rate hikes.

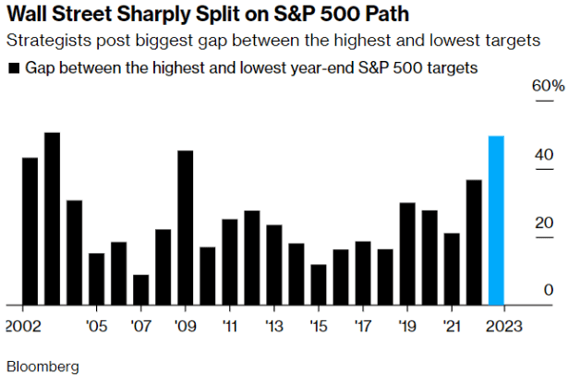

Outlook: Planning for the best – or the worst

Some investors expect the mega cap technology names to drive the market to further gains. Others expect a recession to result in losses.

This has led to a very wide divergence among views on Wall Street. The most optimistic forecast is for a further 10% gain, while the most negative forecast is for a 27% loss in the second half [2]The chart below shows that this is one of the widest ranges of Wall Street forecast we’ve seen in some years.

Tune into our Q3 market update webinar on July 18 to learn how we are managing through this uncertainty. Register

Big difference between bulls and bears[3]

This material is intended to be educational in nature,[4] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: Bloomberg, S&P Global manufacturing purchasing managers index data

[2] Source: Bloomberg Wall Street Forecasters, Blindsided by Tech Stock Rally, Divided on 2023 Outlook - Bloomberg

[3] Source: Bloomberg Wall Street Forecasters, Blindsided by Tech Stock Rally, Divided on 2023 Outlook - Bloomberg

[4] Source: Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggretate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

OAI00326

{kind=link}