April 25, 2022 •OneAscent

Both equity and fixed income markets continued their downward slide last week. The war in Ukraine continues to drag on, Covid-19 lockdowns in China persist, and Federal Reserve President Powell indicated that a 50-bps interest rate increase is “on the table” at the next meeting.[1] The S&P 500, a proxy for US large-cap stocks, fell 2.7 percent for the week, bringing year-to-date losses to ten percent. The Bloomberg US Aggregate Bond index, a proxy for investment grade US bonds, dropped approximately one percent, bringing year-to-date losses to 9.5%.[2]

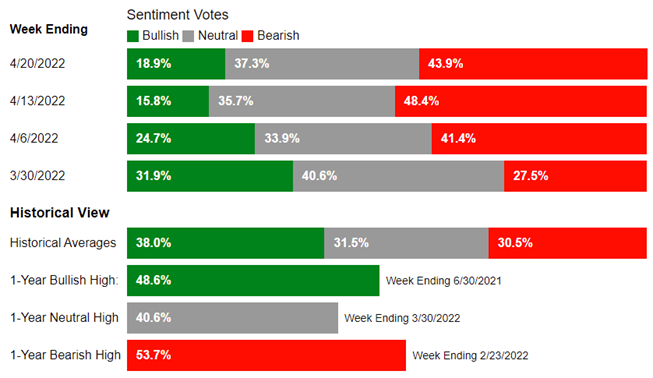

The persist negative news to begin the year has clearly weighed on investor sentiment. The American Association of Individual Investors asks investors each week if the stock market will be higher (bullish), the same (neutral), or lower (bearish) in six months. Of all those surveyed, bullish investors (18.9%) remain significantly lower than the long-term average (38%). In fact, this most recent weekly reading marks the first time since May of 2016 that bullish investors have been below 20% for consecutive weeks.

However, there may be a potential silver lining to these negative sentiment readings. “Historically, the S&P 500 index has gone on to realize above-average and above-median returns during the six- and 12-month periods following unusually low readings for bullish sentiment."[3]

Prices & Interest Rates

| Representative Index | Current | Year-End 2021 |

|---|---|---|

| Crude Oil (US WTI) | $104.56 | $75.37 |

| Gold | $1,930 | $1,828 |

| US Dollar | 101.12 | 95.67 |

| 2 Year Treasury | 2.72% | 0.73% |

| 10 Year Treasury | 2.90% | 1.52% |

| 30 Year Treasury | 2.95% | 1.93% |

| Source: Morningstar, YCharts, and US Treasury as of April 24, 2022 |

Asset Class Returns

| Category | Representative Index | YTD 2022 | Full Year 2021 |

|---|---|---|---|

| Global Equity | MSCI All-Country World | -10.6% | 18.5% |

| Global Equity | MSCI All-Country World ESG Leaders | -11.7% | 20.8% |

| US Large Cap Equity | S&P 500 | -10.0% | 28.7% |

| US Large Cap Equity | Dow Jones Industrial Average | -6.4% | 21.0% |

| US Small Cap Equity | Russell 2000 | -13.3% | 14.8% |

| Foreign Developed Equity | MSCI EAFE | -10.0% | 11.3% |

| Emerging Market Equity | MSCI Emerging Markets | -12.2% | -2.5% |

| US Fixed Income | Bloomberg Barclays Municipal Bond | -8.6% | 1.5% |

| US Fixed Income | Bloomberg Barclays US Agg Bond | -9.5% | -1.5% |

| Global Fixed Income | Bloomberg Barclays Global Agg. Bond | -10.4% | -4.7% |

| Source: YCharts as of April 24, 2022 | |||

[1] Source: Wall Street dives, dollar jumps as rate hikes take spotlight | Reuters

[2] Source: YCharts

[3] Source: AAII Sentiment Survey: Bullish Sentiment Stays Below 20% for a Second Week | AAII

Download PDF Version

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data. Please contact your Financial Advisor in order to complete an updated risk assessment to ensure that your investment allocation is appropriate.