August 8, 2022 •Nathan Willis

"We are in danger of having the worst banana in 45 years”

Alfred Kahn, President Jimmy Carter’s “Inflation Czar”, uttered this phrase in 1978 after he infuriated the president by pointing out the possibility of a recession. Thereafter, Kahn stopped using the word ‘recession’ and took to calling it a banana to soften the blow.[1]

After the hyperinflation of the 70s and 80s, the “recession” word is still loathed; At the turn of the century, White House advisors in the West Wing television show referred to recessions as “bagels,”[2] and Treasury Secretary Janet Yellen recently said the economy is “in transition.”[3]

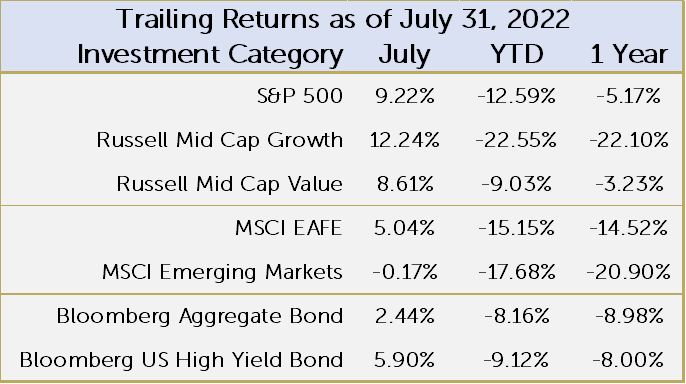

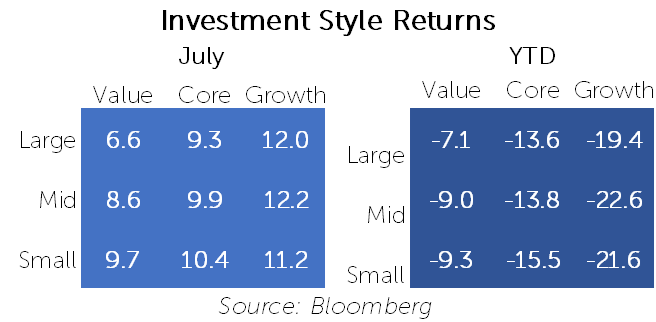

During July, the markets processed the odds of recession and the Federal reserve’s (seemingly) dovish shift. In the chart of market returns to the right, you see market’s reaction. A couple things stick out:

One of the fundamental drivers of the strong July returns was the perception that the Fed may slow down its future interest rate hikes. At the press conference following the July 27 Federal Reserve meeting, Governor Powell said “…the pace of those increases will continue to depend on the incoming data and the evolving outlook for the economy.”

The market seized on the ‘data dependent’ wording, which has been used in the past, and the S&P 500 index rose 1.3% from the beginning of the press conference through the rest of the day. Indeed, the last three days of the month drove much of July’s solid returns.

What does the Fed’s decision and outlook mean for the markets? Is the economy headed for a recession and, if so, what should we expect? How should we position our portfolios?

Our discipline is to use our Navigator process, focused on a data-driven review of Valuation, the Economy, Technical and Sentiment factors. Over the last couple of months, we have seen some changes.

Valuation: For the first time in over two years, valuation is not a negative. Stocks have become cheaper. At the same time, yields have risen, making bonds–especially corporate bonds–more attractive than they have been since the pandemic.

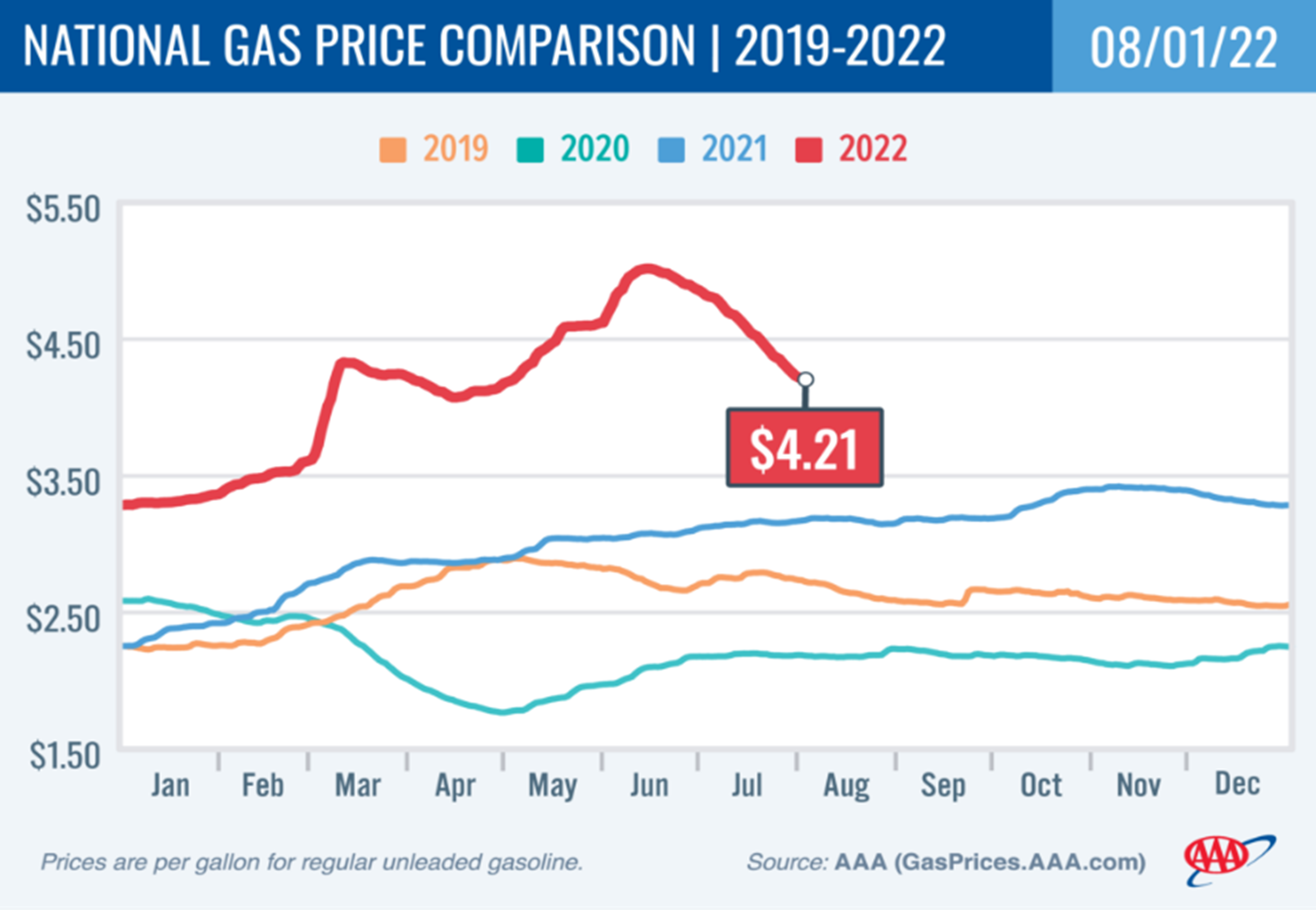

Economy: The economy is a mixed bag with some pockets of strength offset by weakness. Employment is strong, with a very low unemployment rate, but real (after inflation) earnings were down 4.4% in July 2022 vs. July 2021.[4] This is important, as the consumer is a key driver of the US economy. Earnings have remained strong even though, as expected, growth has moderated from the stunning profit growth of 2021. Earnings estimates for 2022 have begun to decline over the last month, and we continue to watch earnings growth closely.[5] One pocket of optimism is the moderation of inflationary pressures. As this chart shows, gasoline prices have dropped over the last month, one of many signs that inflation is beginning to moderate.

Economy: The economy is a mixed bag with some pockets of strength offset by weakness. Employment is strong, with a very low unemployment rate, but real (after inflation) earnings were down 4.4% in July 2022 vs. July 2021.[4] This is important, as the consumer is a key driver of the US economy. Earnings have remained strong even though, as expected, growth has moderated from the stunning profit growth of 2021. Earnings estimates for 2022 have begun to decline over the last month, and we continue to watch earnings growth closely.[5] One pocket of optimism is the moderation of inflationary pressures. As this chart shows, gasoline prices have dropped over the last month, one of many signs that inflation is beginning to moderate.

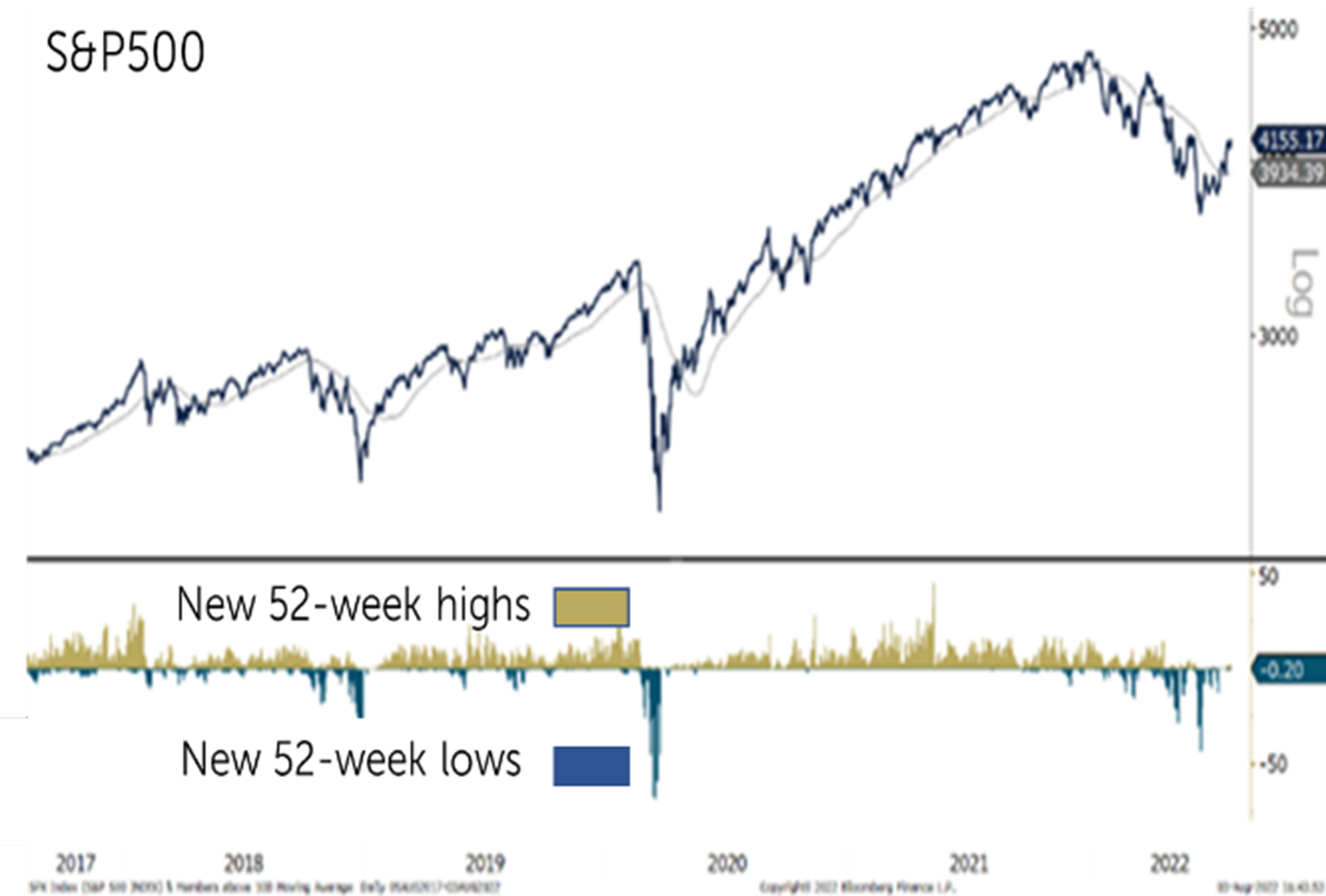

Technicals: Short-term technicals have indicated that the market is stabilizing and beginning to form positive trends. One example, shown in the chart to the left, is that the number of new 52-week lows has begun to decrease. The number of stocks making new lows, represented by blue columns in the lower panel, has declined. This number has spiked during most downturns, and a reduction in new lows–as well as an increase in new highs, noted by the brown columns–would help to confirm a positive trend in the stock market.

Technicals: Short-term technicals have indicated that the market is stabilizing and beginning to form positive trends. One example, shown in the chart to the left, is that the number of new 52-week lows has begun to decrease. The number of stocks making new lows, represented by blue columns in the lower panel, has declined. This number has spiked during most downturns, and a reduction in new lows–as well as an increase in new highs, noted by the brown columns–would help to confirm a positive trend in the stock market.

Sentiment: The American Association of Individual Investors survey is a well-known metric that we view as a contrarian indicator; when investors are negative on the stock market, that often means that the clouds contain silver linings. We see that situation today as the AAII survey bull minus bear measure has been negative for several weeks.[6]

In today’s environment it pays to remember the quote that we published in our quarterly call presentation. Economist Paul Samuelson once said: “Stocks have predicted 9 out of the last 5 recessions.” Maintaining discipline, free from distraction and focused on maximizing potential opportunity, is key.

So, we have recently taken some portfolio actions worth mentioning:

In conclusion, don’t think that we will “slip on a banana.” Considering many improving and positive indicators in the market, the possibility of a recession is not the only outcome on which to concentrate. As we finish out the summer, we remind ourselves that the greatest chance of success lies in maintaining our discipline and sticking with our plans, and we urge our partners to do the same. Returns may even turn out to be "a-peel-ing," so to speak. 🍌

[1] Time Magazine, Dec 11,1978 Business: Yes, We Have No Bananas - TIME

[2] “7A WF 83429”, The West Wing, created by Aaron Sorkin, Season 5, Episode 1, NBC, 2003

[3] Janet Yellen, Remarks by Secretary of the Treasury Janet L. Yellen at White House Virtual Roundtable with Business and Labor Leaders | U.S. Department of the Treasury, August 4, 2022, https://home.treasury.gov/news/press-releases/jy0915

[4] Bureau of Labor Statistics

[5] Bloomberg

[6] American Association of Individual Investors

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.