June 6, 2023 •Nathan Willis

![]() Nathan: Write me a two-sentence summary of what has driven tech stock returns this year.

Nathan: Write me a two-sentence summary of what has driven tech stock returns this year.

![]() ChatGPT: Tech stock returns have been primarily driven by factors such as increased demand for tech products and services due to digital transformation, low interest rates prompting investors to seek higher returns, and the accelerated adoption of remote work and digital solutions during the pandemic. Additionally, ongoing innovation in emerging technologies and the long-term growth potential of the sector have contributed to the strong performance of tech stocks this year.[1]

ChatGPT: Tech stock returns have been primarily driven by factors such as increased demand for tech products and services due to digital transformation, low interest rates prompting investors to seek higher returns, and the accelerated adoption of remote work and digital solutions during the pandemic. Additionally, ongoing innovation in emerging technologies and the long-term growth potential of the sector have contributed to the strong performance of tech stocks this year.[1]

If generative artificial intelligence is capable of writing part of this commentary, then maybe it can be the catalyst for a renaissance in American technological superiority.

Optimism about this potential has driven a massive rally in mega-cap technology stocks this year. The S&P 500 technology index is up 32% YTD, and though the market-cap-weighted S&P 500 is up 10%, the equal-weighted version of the index is actually down for the year.[2]

Technology is the story today. But is its performance justified, and will it continue?

Before we develop a structure for answering these questions, let’s review market returns in more depth.

Worries about the banking system and debt ceiling debate faded into the background as technology drove returns. Narrow market leadership contradicted mediocre returns outside the mega-caps:

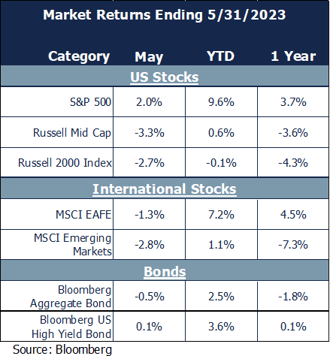

The S&P 500 led the way, up 2% in May. Nearly all other equities struggled:

The headline S&P 500 return appears great. Add to that the fact that the VIX, a measure of equity volatility, is at its lowest level since the pandemic[4] and the outlook appears strong. Under the surface, however, markets may not be so sanguine.

We follow our Navigator process to maintain discipline and perspective. Let’s use the process to sort through the noise.

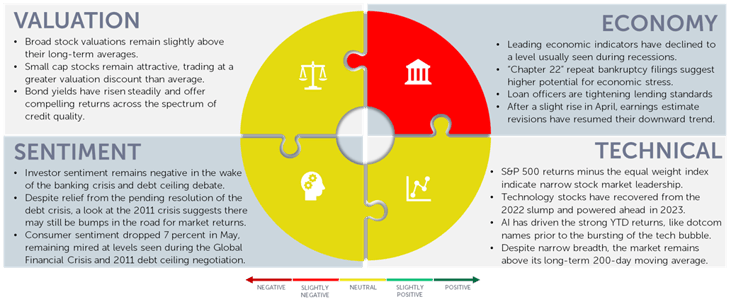

Economy: Leading economic indicators have declined to a level that suggests a formal recession is imminent. Additionally, corporate balance sheets may be strained: The level of “Chapter 22” repeat bankruptcies has reached its highest level outside of 2009, and banks are tightening lending standards to levels only seen during the tech bubble, 2008 crisis, and the pandemic. Finally, earnings estimates have resumed their decline after an April respite.

Technicals: The market is exhibiting narrow breadth, a situation which historically has preceded mediocre returns:

Despite these concerns, the market remains solidly above its 200-day moving average, a significant level of technical support.

Sentiment: Investor sentiment remains quite negative, which is a positive for stock returns. A resolution of the debt ceiling, however, may not improve the outlook; stocks still lost money after the 2011 debt ceiling crisis was resolved. Finally, consumer sentiment has dropped to levels seen during the 2008 financial crisis.

Valuation: US stock market valuations have recovered and now sit modestly above long-term averages. Small cap and international stocks, however, remain at a valuation discount relative to US large cap stocks. Most bond sectors are attractive both relative to their recent history and relative to stocks, as yields have risen again.

Investor optimism surrounding AI’s potential has moved the debt ceiling and banking crisis into the rearview mirror. Many conflicting signals compete for investors’ attention. The prudent course is to remain disciplined.

Therefore, we recommend that investors:

Despite the high likelihood of short-term market volatility, confidence in a plan and investment strategy that works for you is vital. We urge investors to talk with your trusted advisor and evaluate your plan.

[1] Source: ChatGPT ChatGPT (openai.com)

[2] Source: Bloomberg

[3] Source: Bloomberg. Growth stocks represented by Russell 3000 Growth index. Value stocks represented by Russell 3000 Value index.

[4] Source: Bloomberg

[5] The “four horsemen” of the tech boom were Microsoft, Intel, Cisco and Dell Is 'FAANG' More Dangerous Than The '4 Horsemen' Of The Late 1990s And The 'Nifty Fifty' Of The Early 1970s? | Nasdaq

[6] Source: Bloomberg

[7] Source: CNBC Big Tech carries market: Seven mega-caps drive rally (cnbc.com)

[8] Source: Bloomberg

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

OAI00300