April 10, 2023 •Nathan Willis

The failure of Silicon Valley Bank (SVB) defined the month of March. SVB was the second largest bank failure in history (Washington Mutual, in 2008, was the largest).[1]

The bank’s deposit growth was turbo-charged by their venture capital-backed clientele. Their balance sheet collapsed when their investments lost value because of inflation and the Fed’s interest rate hikes, which triggered an old-fashioned bank run, leading to the bank’s demise.[2]Just like any other bank run, depositors and investors lost confidence in the bank. Confidence is the most important ingredient for the US banking system. More on that later.

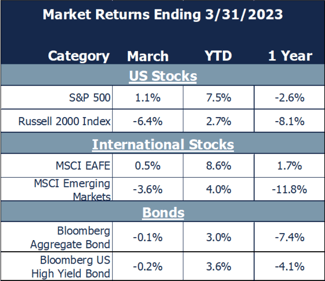

Despite the banking crisis and the steady drumbeat of companies downgrading their expectations for 2023 earnings, the S&P 500 actually gained 1.1% during March, bringing YTD gains to 7.5%. Most other markets, though, didn’t fare quite as well.

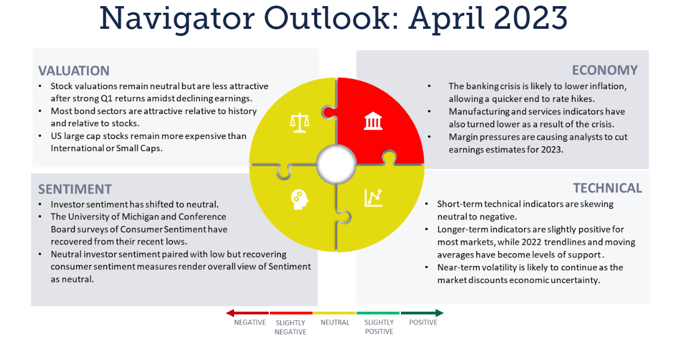

We follow our Navigator process to maintain discipline and perspective. Let’s review what it is telling us.

Valuation: S&P 500 valuations remain in the neutral zone, close to their 25-year average but less attractive after strong first quarter returns amidst declining earnings estimates. Most bond sectors are attractive relative to their recent history and relative to stocks. The earnings yield (the inverse of the price/earnings ratio) of the US large cap stock market is very close to the yield of the bond market after having been at a significant premium for the last ten years; stocks have not been this expensive relative to bonds in some time. US large cap stocks also remain more expensive than international and small cap stocks.

Economy: Outside of calls for greater regulation, the most likely result of the banking crisis is a worse economic slowdown; the Institute for Supply Management survey of new orders dropped to 44 in March as the economy began to react to the banking crisis. We expect further slowing as bank lending standards have tightened.

Technicals: Technical indicators are neutral overall for stocks. Short-term technical indicators remain negative, and volatility has increased. Markets seem to have some intermediate to long-term support after moving above the 2022 downtrends.

Sentiment: Investor sentiment has moved into a more neutral range. Investor sentiment has become more evenly balanced after remaining quite negative for over a year, reducing the optimistic tone of this contrarian indicator. Consumer surveys have moved off their lows after bottoming last year.

We enter April with a mix of optimism and pessimism. As the banking crisis began to slow the economy during March, we can expect inflation to slow as well, bringing the cycle of interest rate hikes to an end sooner rather than later. Pessimism results as much from what we don’t know as with what we do know. The economy is likely to slow more than we expected prior to the crisis, but how much slower is uncertain. However, the market often sees beyond short-term fluctuations in the economy, and it is wise for investors to do so as well.

We recommend investors:

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

OAI00225