February 7, 2023 •Nathan Willis

The markets breathed a sigh of relief in January. After finishing a difficult 2022 they launched into the new year on hopes for a “goldilocks” economy – not too hot, not too cold. Two senior Fed officials set the stage for strong gains by indicating that continued evidence of cooling inflation might allow them to pause interest rate hikes following their next meeting, to be held in March.

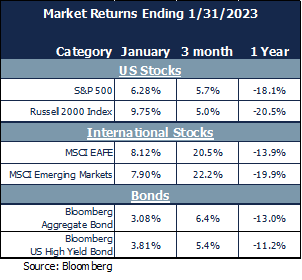

The S&P 500 gained 6.28% during January. International stocks continued their fourth quarter outperformance as the MSCI EAFE finished up 8.12% while emerging markets stocks earned 9.21%. US bonds also recovered solidly; the Bloomberg Barclay’s Aggregate index earned 3.08% for the month and high yield bonds outperformed, indicating recession fears have subsided.

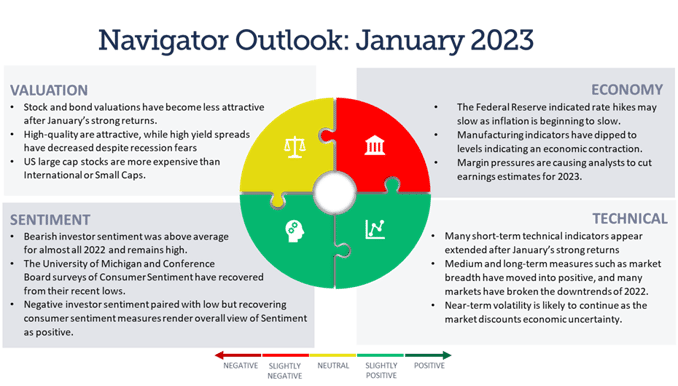

In order to maintain discipline and perspective, we use our Navigator process. Let’s review what it is telling us.

Valuation: The sharp run-up during January has taken the S&P 500 valuation to 18x, back above the 25-year average. International and small caps remain less expensive than US large cap stocks, and value stocks remain less expensive than growth-oriented names. Fixed income spreads have shrunk as well, making bonds less attractive. Valuations are neutral, but not far from moving into negative territory.

Economy: The ISM (Institute for Supply Management) survey of new orders declined to 42.5 in January, as the anticipated slowdown affected corporate spending. The two times this measure has been lower in the last 20 years were during the pandemic and the Global Financial Crisis. We have been monitoring earnings, specifically profit margins, and they are declining as expected based on new orders data.

Economic indicators are negative; the caveat to this negativity is that a recession is the consensus on Wall Street. We are not predicting that we avoid one, but one data point that we have highlighted in the past is high yield spreads, which remain low.

Investors in these bonds are not requiring the extra income investors usually require when a recession, and corporate bond defaults, are on the horizon.

Technicals: Short-term measures have begun to show some fatigue during January, but medium-term and long-term indicators are positive. Market breadth is still quite strong, and many markets appear to have broken 2022 downtrends. Technicals are modestly positive.

Sentiment: Investor sentiment has been negative since the summer, and this contrarian indicator, combined with recovering consumer sentiment, is positive.

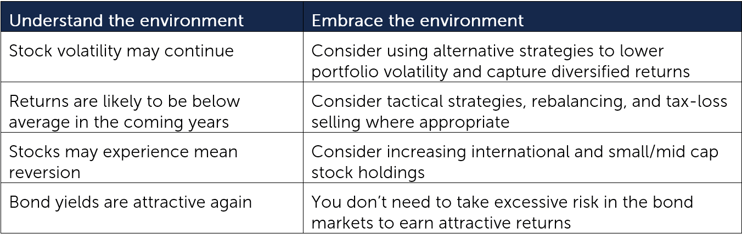

Economic data weakened during the month of January, while the stock and bond markets exhibited strong returns across the board. What is an investor to do in this kind of environment of uncertainty?

One answer is to recall that the stock market is a discounting mechanism – all the information that we know for sure tends to be reflected in market returns. Wall street knows (or thinks it knows – Fed Chairman Powell is not as certain) that we’ll have a recession in 2023 and the Fed will come to the rescue by lowering interest rates. If that is the case, the market is simply looking past the recession and downturn in profits, and anticipating business will get back on track. While we all like to think we’re long-term investors, it is easy to let emotions get us off-track in the short term.

OneAscent uses our Navigator process to illuminate the path forward in uncertain environments like today’s. Here are some recommendations from our quarterly call, held in January, that still hold true:

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

OAI00182