September 1, 2022 •OneAscent

The old investing adage, “don’t fight the Fed”, was in full force in August as both stocks and bonds declined after hearing a more resolute tone from Federal Reserve Chair, Jerome Powell, regarding the path of interest rate hikes in pursuit of blunting inflation. A subsection of that speech is below (our emphasis added): “Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain." [1]

We believe that, in many ways, the inflation-fighting pursuit of the Fed is just. However, their tools are certainly limited. Higher interest rates do not produce more energy for Europe in the midst of a potential standoff with Russia. Nor do they produce greater agricultural output during extreme weather conditions. The Fed can only seek to reduce demand, but increasing supply takes time, investment, and innovation.

|

|

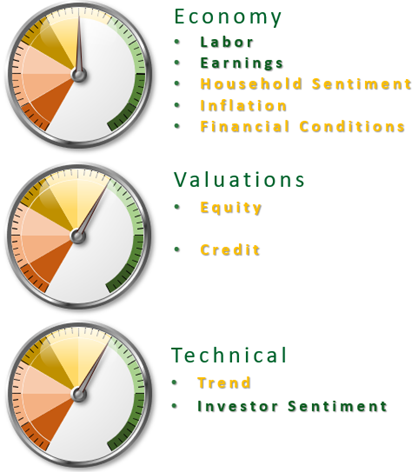

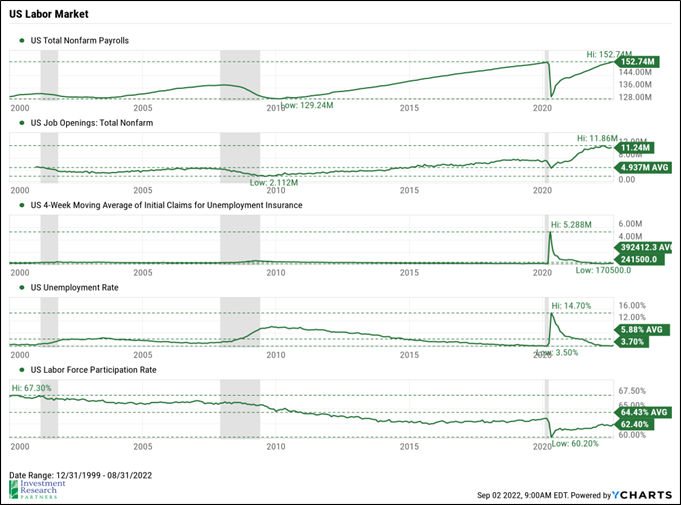

Labor Market

The labor market remained a pillar of strength for the economy through the month. Total US payrolls reached an all-time high in July and the unemployment rate, while ticking up slightly to 3.7% in August, remains well below average since 2000. Job openings remain plentiful (nearly two openings for every person seeking a job) and initial claims for unemployment insurance are below average. If there is a recession on the horizon, it’s not being reflected in the labor market thus far. We will be watching to see if continued Federal Reserve hawkishness leads to a slowdown in hiring.

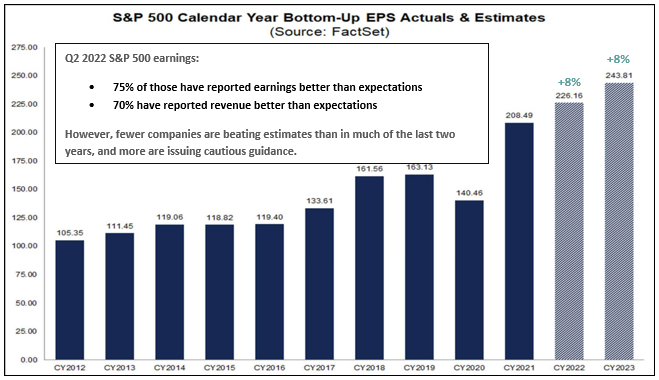

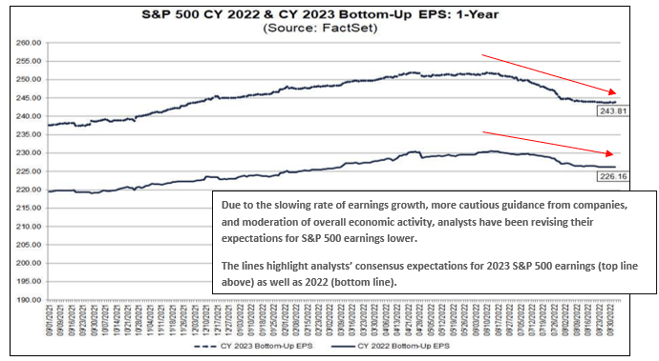

Corporate Earnings

Large US companies have largely managed through the various challenges of 2022 reasonably well. S&P 500 earnings have continued to increase, albeit at a slower pace than originally expected, which has likely contributed to share price declines this year.

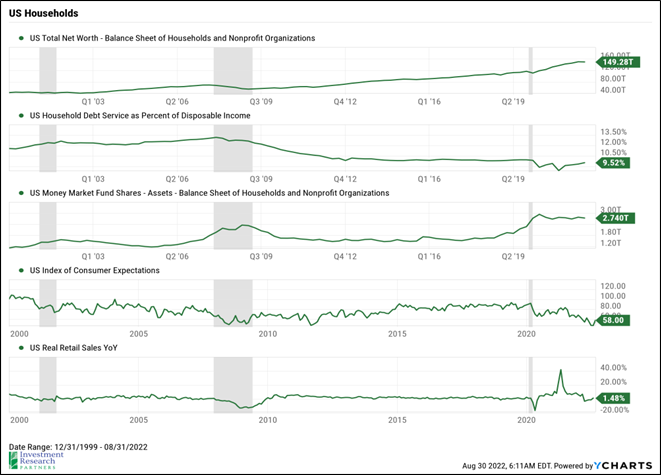

Households

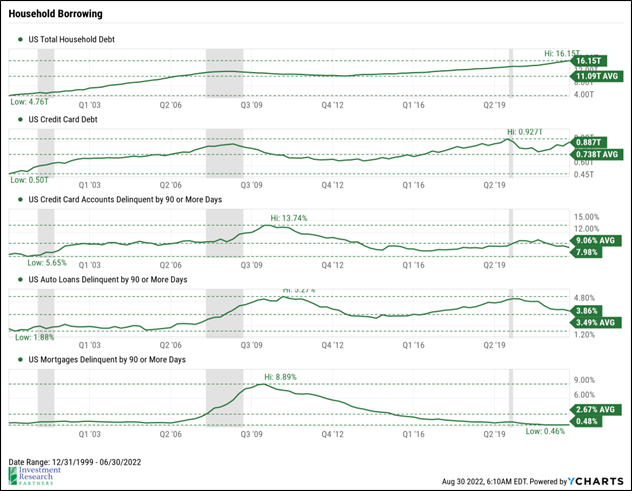

Another pillar of strength for the US economy is household finances, which are in relatively good shape, on average, driven by increased home equity, investment balances, cash balances, and higher wages. However, inflation and the potential for eroding living standards, has pushed household sentiment to its lowest levels in decades, potentially implying a slowdown in discretionary spending activity. Household debt has begun to rise, but delinquency rates are below average, particularly mortgage delinquencies.

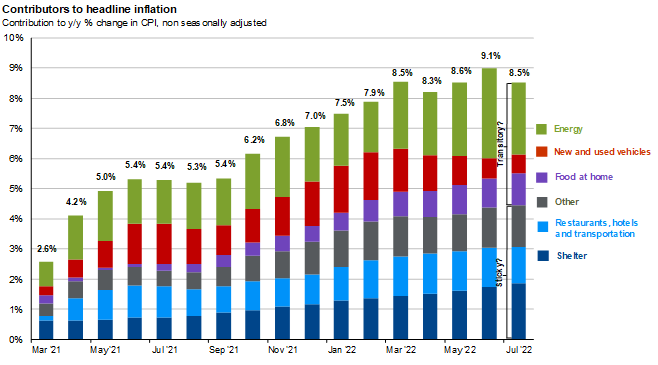

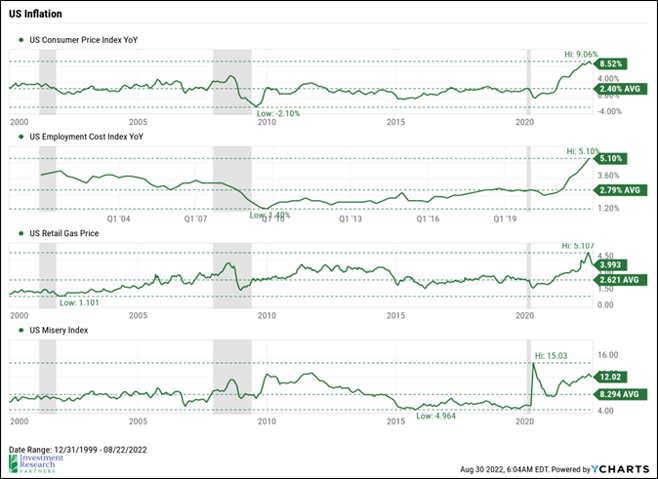

Inflation Higher costs have plagued markets, households, and businesses for much of the last year. The pandemic caused supply and demand imbalances that still persist today, low interest rates drove a significant increase in home prices, and a large number of workers leaving the labor force has led to higher employment costs for businesses. On top of all this, the war in Ukraine has significantly increased the costs of food and energy. Importantly, we’ve begun to see some slowing the pace of rising costs as mortgage rates have increased and additional energy production has come online.

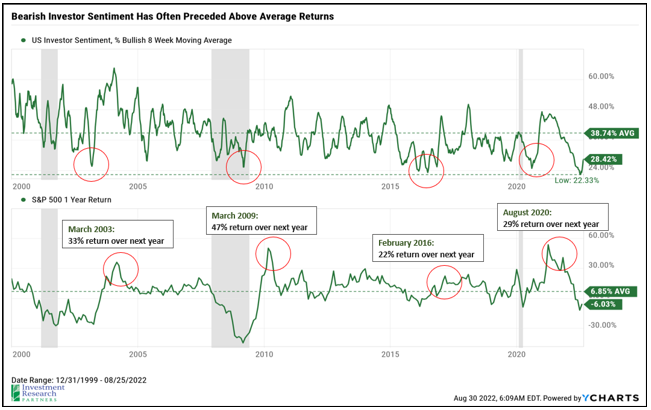

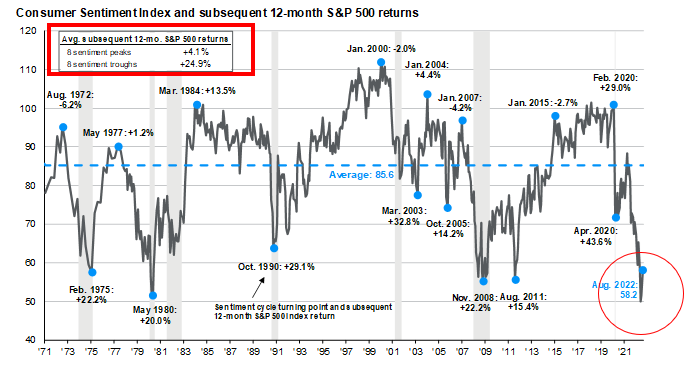

Sentiment.

Both investor sentiment and household sentiment remain extremely low. While not a perfect timing tool, investing during environments like the one we’re in today have often led to above average future returns.

Prices & Interest Rates

| Representative Index | August 2022 | Year-End 2021 |

|---|---|---|

| Crude Oil (US WTI) | $89.55 | $75.21 |

| Gold | $1,713 | $1,828 |

| US Dollar | 108.75 | 95.97 |

| 2 Year Treasury | 3.45% | 0.73% |

| 10 Year Treasury | 3.15% | 1.52% |

| 30 Year Treasury | 3.27% | 1.90% |

| Source: Morningstar, YCharts, and US Treasury as of August 31, 2022 |

Asset Class Returns

| Category | Representative Index | May 2022 | YTD 2022 |

|---|---|---|---|

| Global Equity | MSCI All-Country World | -3.7% | -17.8% |

| Global Equity | MSCI All-Country World ESG Leaders | -4.5% | -19.7% |

| US Large Cap Equity | S&P 500 | -4.1% | -16.1% |

| US Large Cap Equity | Dow Jones Industrial Average | -3.7% | -12.0% |

| US All Cap Equity | Russell 3000 Growth | -4.4% | -23.1% |

| US All Cap Equity | Russell 3000 Value | -3.0% | -10.0% |

| US Small Cap Equity | Russell 2000 | -2.1% | -17.2% |

| Foreign Developed Equity | MSCI EAFE | -4.8% | -19.6% |

| Emerging Market Equity | MSCI Emerging Markets | 0.4% | -17.5% |

| US Fixed Income | Bloomberg Barclays Municipal Bond | -2.2% | -8.6% |

| US Fixed Income | Bloomberg Barclays US Agg Bond | -2.8% | -10.8% |

| Global Fixed Income | Bloomberg Barclays Global Agg. Bond | -4.0% | -15.6% |

| Source: Morningstar, YCharts, and US Treasury as of August 31, 2022 | |||

[1] Powell sees pain ahead as Fed sticks to the fast lane to beat inflation | Reuters

Download PDF Version

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data. Please contact your Financial Advisor in order to complete an updated risk assessment to ensure that your investment allocation is appropriate.