June 1, 2021 •OneAscent

|

|

We monitor the backdrop for investing in risk assets across three primary pillars: economic conditions, asset prices, and technical considerations such as investor sentiment. On balance, we still believe that conditions are favorable for accepting investment risk, but above average asset class valuations and the potential for above-trend inflation should give pause.

For example, economic conditions are very favorable with the labor market improving (and continued room for hiring) and corporate earnings are trending higher. In addition, household balance sheets are healthy, partially thanks to the unprecedented level of support from the federal government and Federal Reserve in the form of direct payments to households, enhanced unemployment benefits, and very low borrowing costs. The above-average rise in prices, particularly related to energy and housing, and accounts of significant supply gaps for manufacturing and construction materials are the one primary concern for the economy today.

This favorable economic and technical backdrop is no secret and is being fully reflected in the price of many assets today. For example, the S&P 500 index has touched multiple all-time highs this year and has already returned 13% through May after returning 18% in 2020[1]. The backdrop is favorable, but asset prices leave little room for error and potentially put investors in a precarious position if economic conditions were to unexpectedly change like they did in early 2020.

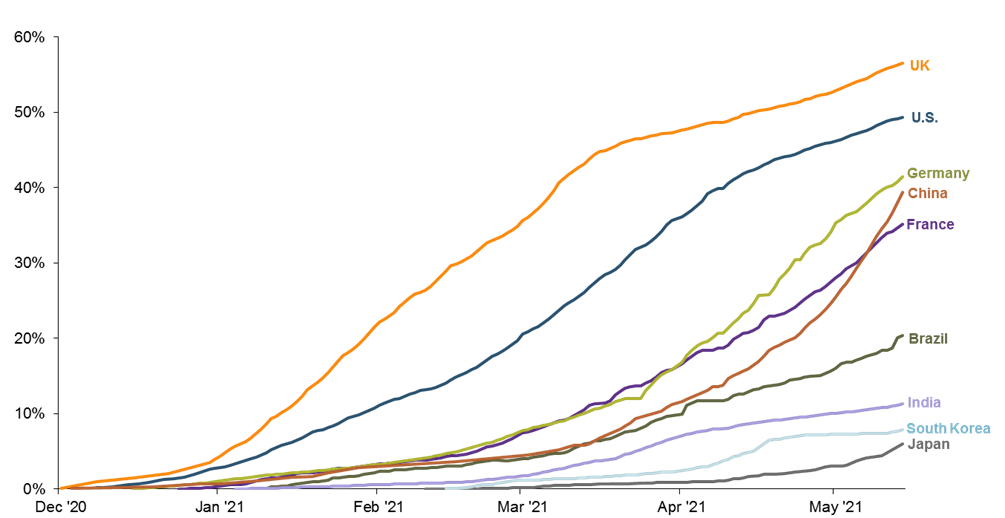

Percentage of Adults that Have Received At Least One Vaccine Dose

The labor market has continued its recovery, though the total number of employed Americans is still below pre-pandemic levels (see chart below). In early June, the US Bureau of Labor Statistics released their monthly assessment of labor market conditions. 559,000 jobs were added to the economy, which was generally in-line with the consensus estimate of economists of 675,000 (source: Bloomberg).

The economy remains more than 8 million jobs short of pre-pandemic levels, which allows significant room for labor market gains before capacity runs out, which has typically been a challenging point in economic cycles as wage inflation may begin to pressure company profitability on average. In May, leisure and hospitality jobs rose by 292,000 following similar gains during the previous two months as a sign that consumers are anxious to resume in-person activities like dining and travel.

Total Non-Farm US Payrolls (millions)

-OneAscent-Financial-Monthly-Investment-Update-June-2021.png)

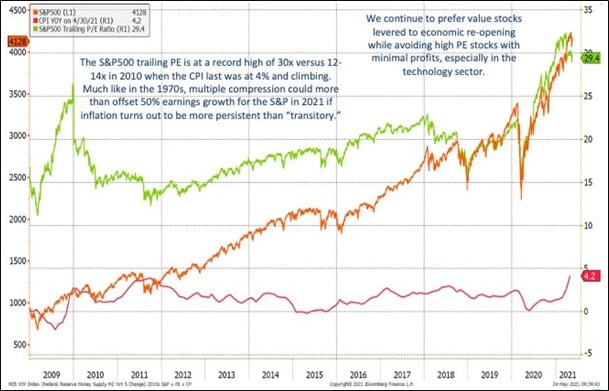

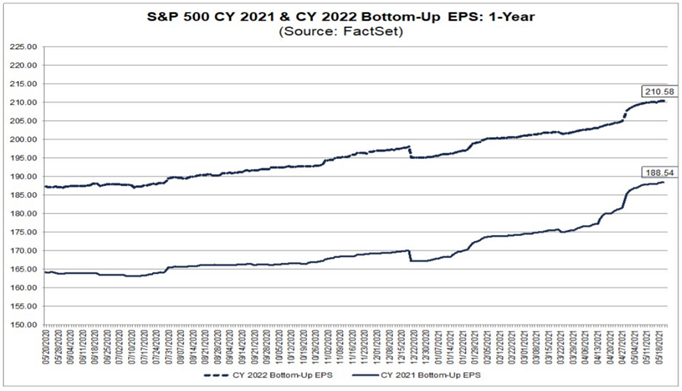

Above average inflation, which has not been a significant concern for most investors in more than a decade is now discussed regularly in the financial media and on corporate earnings calls. While companies and households have witnessed meaningful increases in the costs of labor, materials, and energy over the last year, we do not anticipate runaway inflation that would cause a collapse in corporate earnings and economic activity anytime soon (like the environment witnessed in the 1970s, as highlighted in the first chart below). However, much of the increase in the price investors have been willing to pay for current and future corporate earnings over the last year may be predicated on a very low interest rate and inflation environment. So, while we do not anticipate a hyper-inflation environment, even a return to normal levels of interest rates and inflation may result in a pricing of risk assets. The second chart below highlights the potentially precarious position of the S&P 500 index, which is trading at nearly 30x its most recent year of earnings. But, as we will see in the next section, corporate earnings have continued to recover at a robust pace and outperform expectations, which also provides support / justification for above-average index prices.

The Interaction Between Inflation and the S&P 500 Index

Given current conditions, we advocate that investors:

Asset Class Returns

| Category | Representative Index | May 2021 | YTD 2021 | Full Year 2020 |

|---|---|---|---|---|

| Global Equity | MSCI All-Country World | 1.6% | 10.8% | 16.3% |

| US Large Cap Equity | S&P 500 | 0.7% | 12.6% | 18.4% |

| US Small Cap Equity | Russell 2000 | 0.2% | 15.3% | 20.0% |

| Foreign Developed Equity | MSCI EAFE | 3.3% | 10.1% | 7.8% |

| Emerging Market Equity | MSCI Emerging Markets | 2.3% | 7.3% | 18.3% |

| US High Yield Fixed Income | ICE BofAML High Yield Bond | 0.3% | 2.3% | 6.2% |

| US Fixed Income | Barclays Aggregate Bond | 0.3% | -2.3% | 7.5% |

| Cash Equivalents | ICE BofAML 3 Mo Deposit | 0.0% | 0.0% | 0.5% |

| Source: Morningstar (total returns shown gross of fees) As of May 31, 2021 |

Prices & Interest Rates

| Representative Index | May 31, 2021 | Year-End 2020 |

|---|---|---|

| S&P 500 | 4,203 | 3,756 |

| Dow Jones Industrial Avg. | 34,513 | 30,606 |

| NASDAQ | 13,687 | 12,888 |

| Crude Oil (US WTI) | $66.32 | $48.42 |

| Gold | $1,903 | $1,902 |

| US Dollar | 90.03 | 89.94 |

| 2 Year Treasury | 0.16% | 0.13% |

| 10 Year Treasury | 1.63% | 0.93% |

| 30 Year Treasury | 2.30% | 1.65% |

| Source: Bloomberg, US Treasury (total returns shown gross of fees) As of May 31, 2021 |

[1]Source: Morningstar

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data. Please contact your Financial Advisor in order to complete an updated risk assessment to ensure that your investment allocation is appropriate.