January 3, 2022 •OneAscent

For many investors, 2021 was a year of robust gains with the S&P 500 index returning nearly 29%, but there was significant dispersion in results across industries and geographies. Areas like emerging markets declined 3% as a category as geopolitical risk in China and pandemic-related challenges continued to weigh on these markets. US bonds experienced their first negative calendar year since 2013 after providing approximately 8% annual returns in 2018 and 2019. Energy was the best performing sector in the US, advancing more than 53% during the year as the pace of the economic reopening and subsequent demand for fuel surprised to the upside. And, despite being in the midst of a global pandemic, biotechnology companies as an industry (healthcare companies on the frontlines of seeking cures for diseases) were surprising flat in 2021.[1] The environment for 2022 is setting up to be an exciting one for active investors willing to step beyond simply owning an S&P 500 index fund.

Baseball Hall-of-Famer, Casey Stengel, said, “Never make predictions, especially about the future.” As investors, we are in the business of making observations and allocating capital accordingly, but typically with much longer time horizons than an individual calendar year. Nevertheless, here are areas to watch in 2022:

What will ultimately impact these areas cannot be known today, but our current “known” risks that are most significant are inflation and geopolitical risks. With respect to inflation, our concern is not runaway inflation like that experienced in the US during the 1970s (conditions are much different today, as described in previous versions of this letter), but rather that higher prices could lead to declining standards of living and a pullback in consumer spending to preserve income and wealth.

On the geopolitical front, the combination of Russia and China taking aggressive military posturing toward their respective neighbors, Ukraine and Taiwan, are of significant concern for global political stability in 2022. Russia proved capable of similar aggression on a smaller scale 7 years ago in Crimea, and China’s rhetoric regarding its rights to Taiwan have become increasingly emboldened at the same time that the nation seems less concerned about blowback from western democracies like the US.

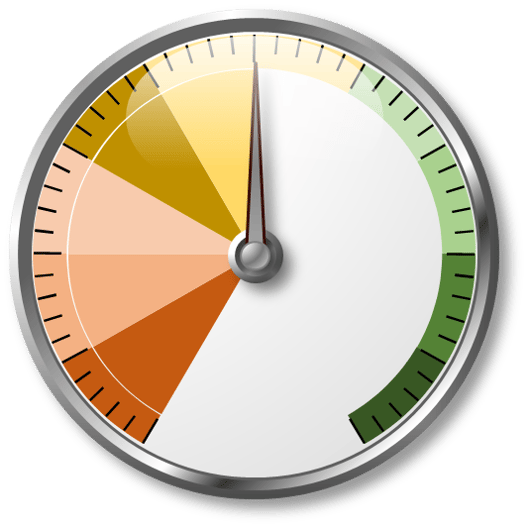

The balance of this letter is in the “usual” format with our risk-taking score and supporting charts on the beginning on the subsequent page. We thank you for reading and we look forward to a bright 2022.

|

|

The Risk-Taking Score (RTS) should be utilized relative to your long-term strategic asset allocation selected by you and your financial advisor. The RTS is meant to be illustrative of our Investment Committee’s view toward the overall investing environment in the short-to-intermediate term (0-3 years) and how your portfolio should be positioned accordingly relative to your long-term strategic allocation.

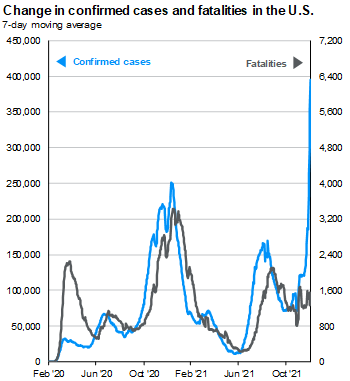

The supporting sections below paint a picture for investing in 2022 that feels very similar to investing in 2021: Economic stability and growth juxtaposed against above-average asset class valuations. Populations in many developed nations began receiving their first dose of COVID-19 vaccinations in early 2021, and now many are receiving their third (booster) dose during a wave of the Omicron variant that appears to be highly transmissible yet less deadly for those who have been vaccinated. Nevertheless, the most recent flare-up in cases seems to be dragging on consumer activity, particularly in the hospitality and travel industries. The key difference at the beginning of 2022 vs. the start to 2021 may be that stimulus and accommodative policies from the US federal government and Federal Reserve are ebbing rather than flowing as these entities seek to pare back pandemic era economic support.

We sincerely believe that 2022 will favor thoughtful asset allocation and stock selection rather than the S&P 500 leading the way yet again. Below are key themes and considerations that we advocate for investors going into 2022. Many of these are holdovers from 2021, and may be even more important in the year ahead:

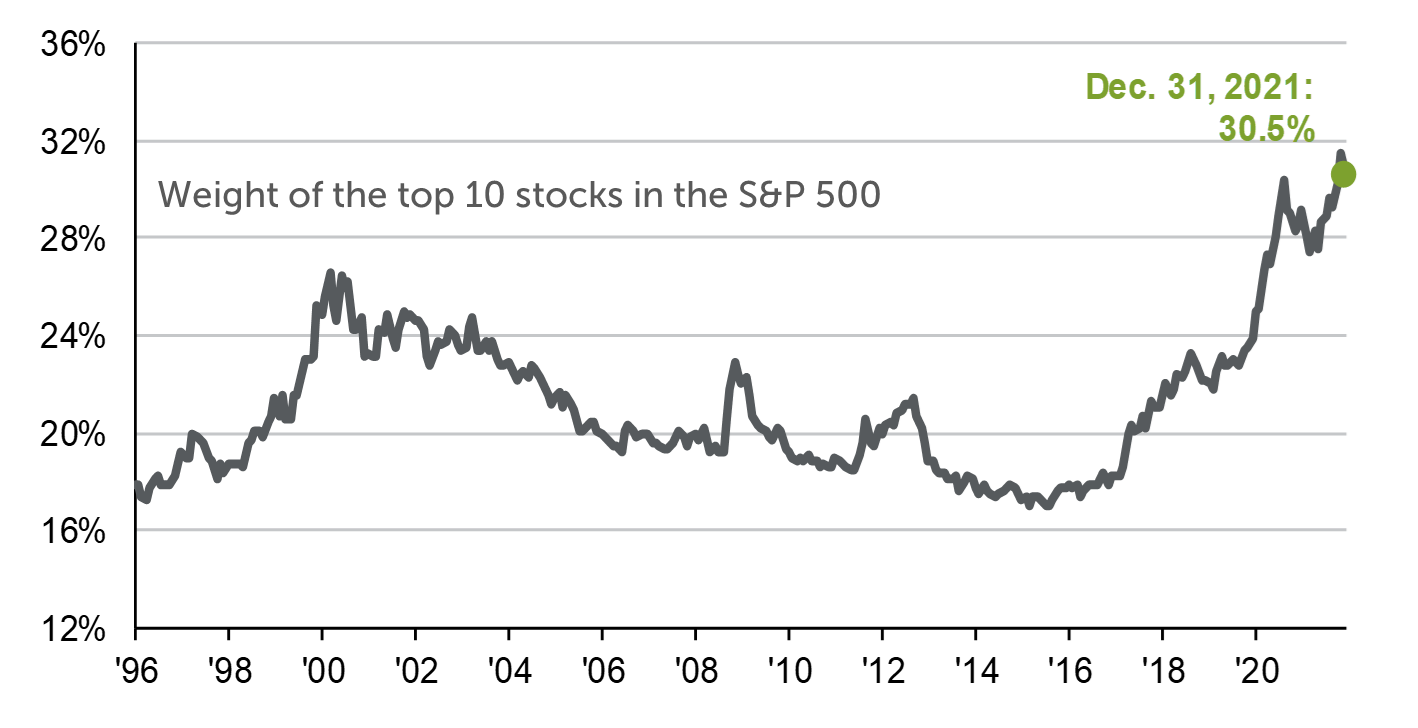

Source: Compustat, FactSet, Standard & Poor’s, J.P. Morgan Asset Management as of December 31, 2021.

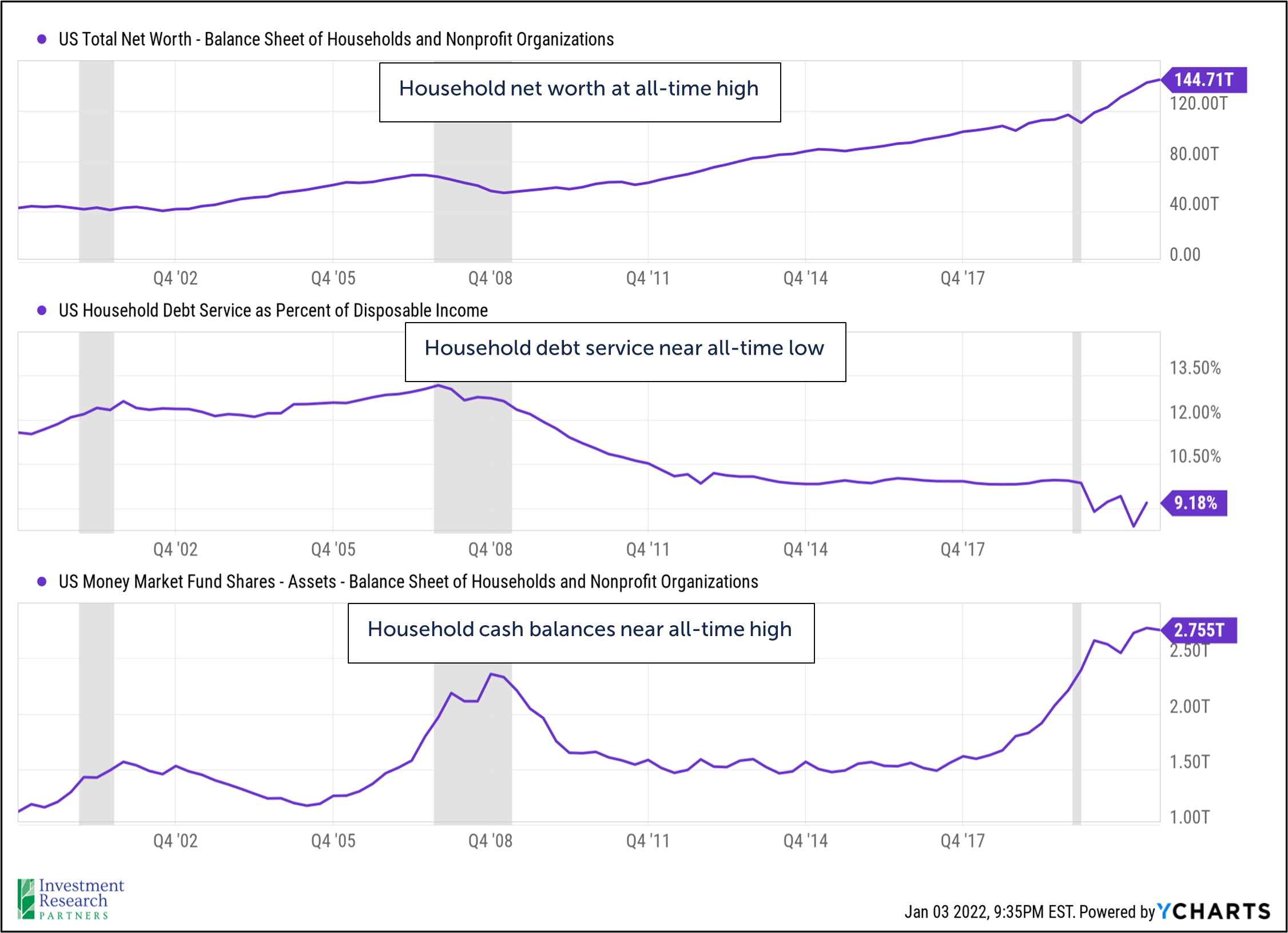

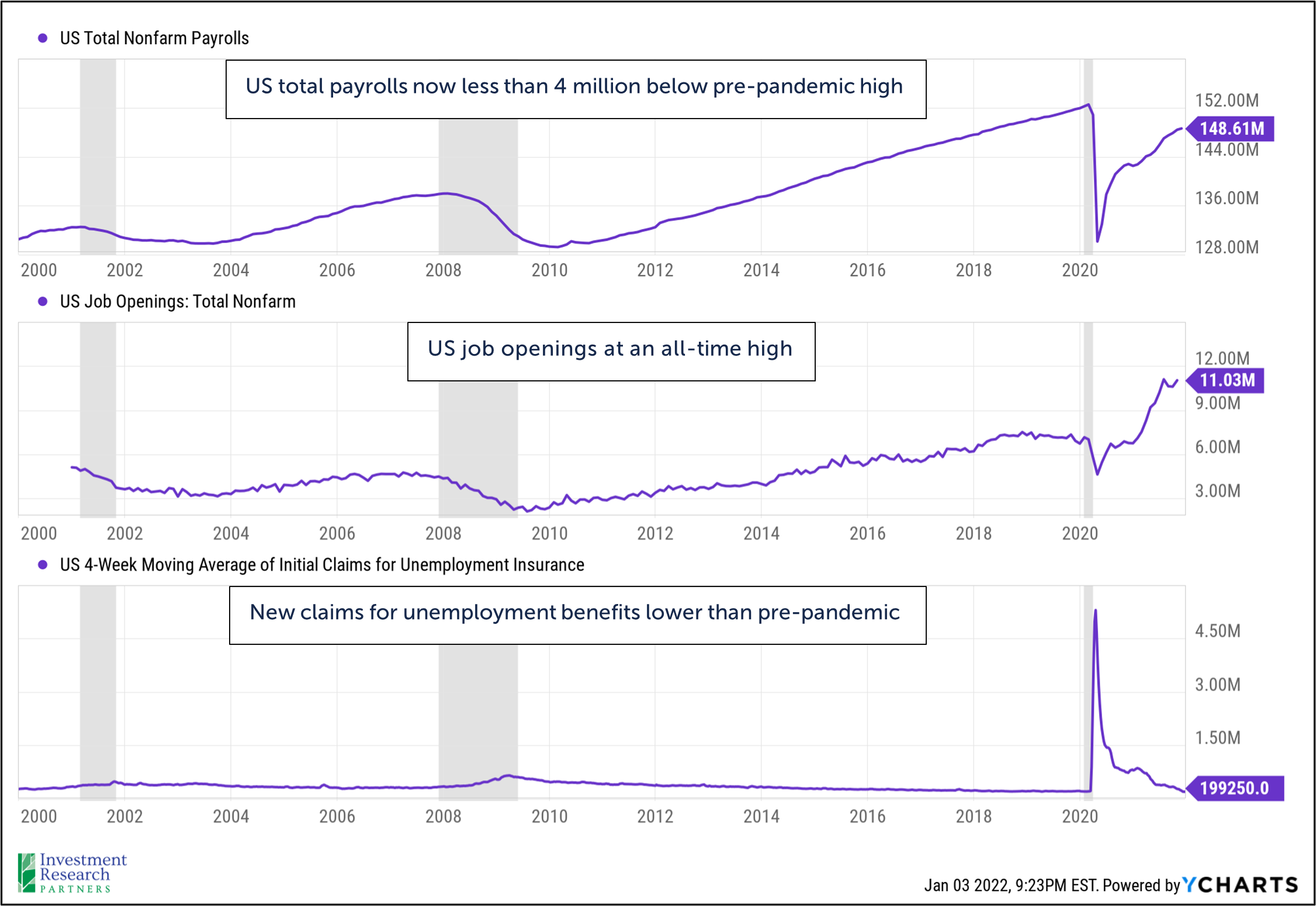

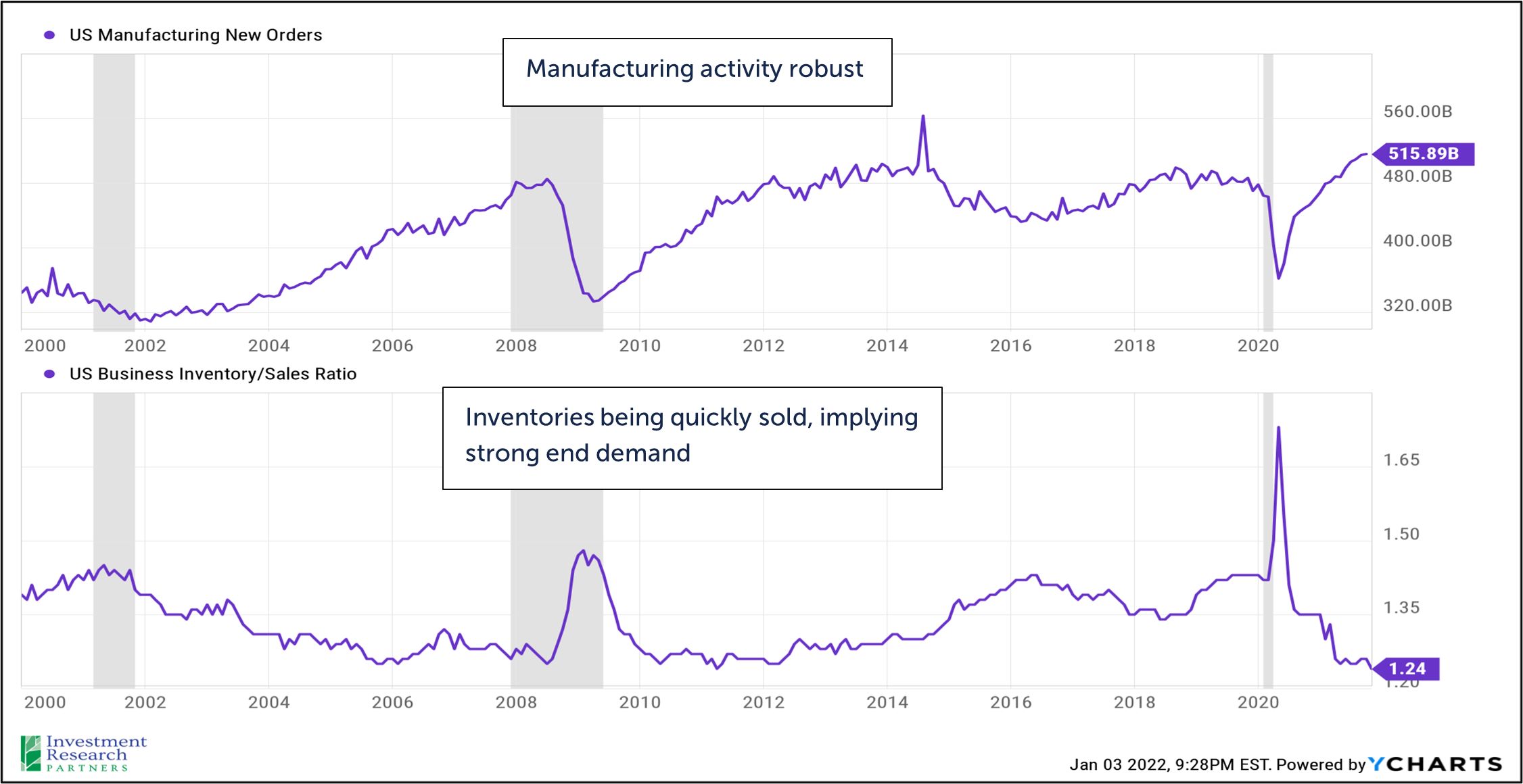

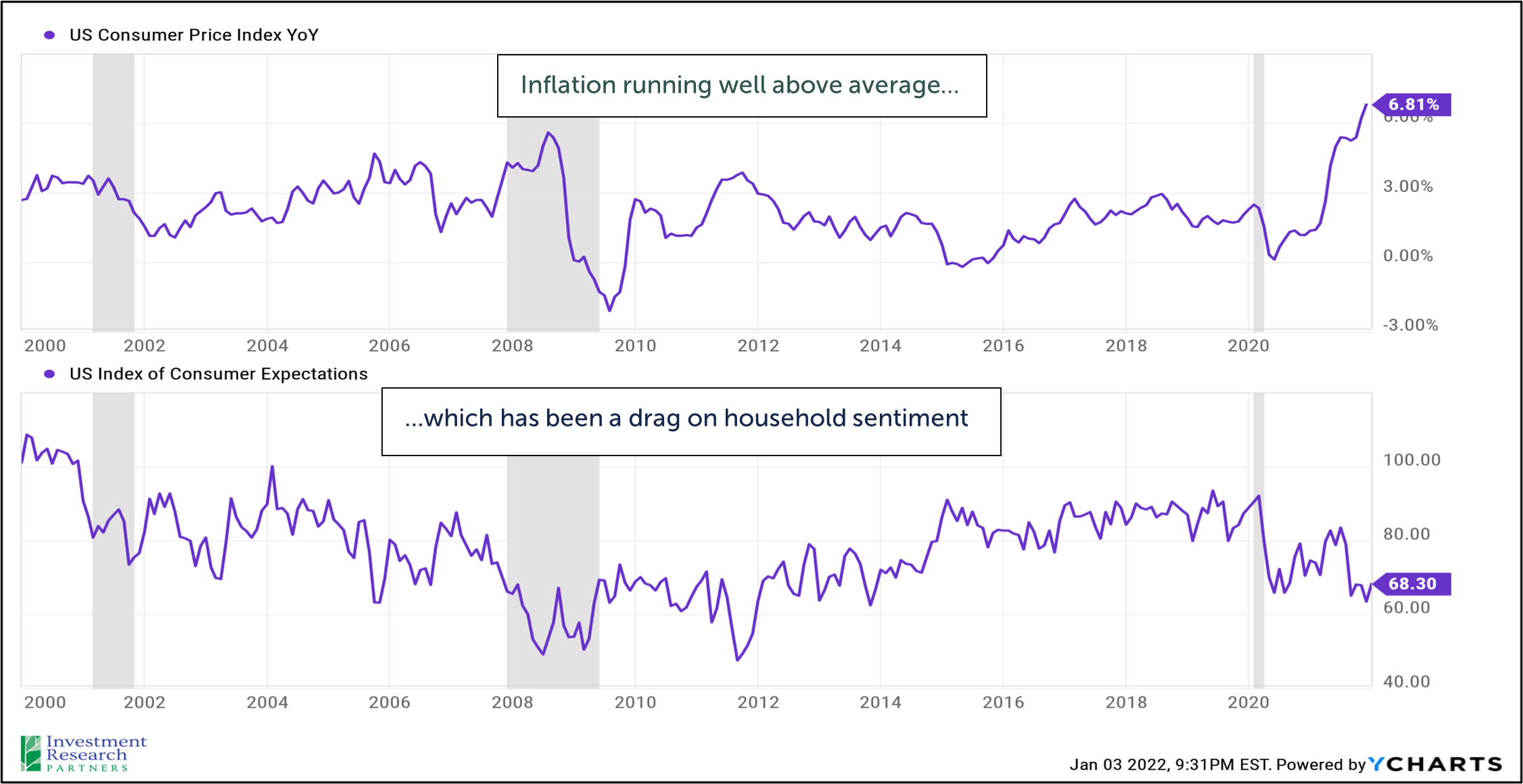

US economic growth remains in an upward trajectory. Inflation and supply chain-related issues continue to receive media attention, but these issues are largely driven by very robust demand for goods and services. Much of this demand is being driven by households which, on average, are in the best financial position in decades as a result of fiscal stimulus and low interest rates. Labor markets have been improving rapidly, with the unemployment rate dropping rapidly to 4.2%, just 0.7% above the 50-year lows set in early 2020. US manufacturing new orders are robust, and we have not yet seen evidence of a concerning build-up in inventories that has predicated past recessions. However, the sharp rise in inflation which began in summer 2021 coincided with a swift reversal of household sentiment as those surveyed responded with concerns that higher prices would erode their standard of living. It will be important to monitor inflation and household sentiment throughout 2022 in order to determine if supply and demand can find a balance without causing American households to simultaneously and meaningfully reduce their spending.

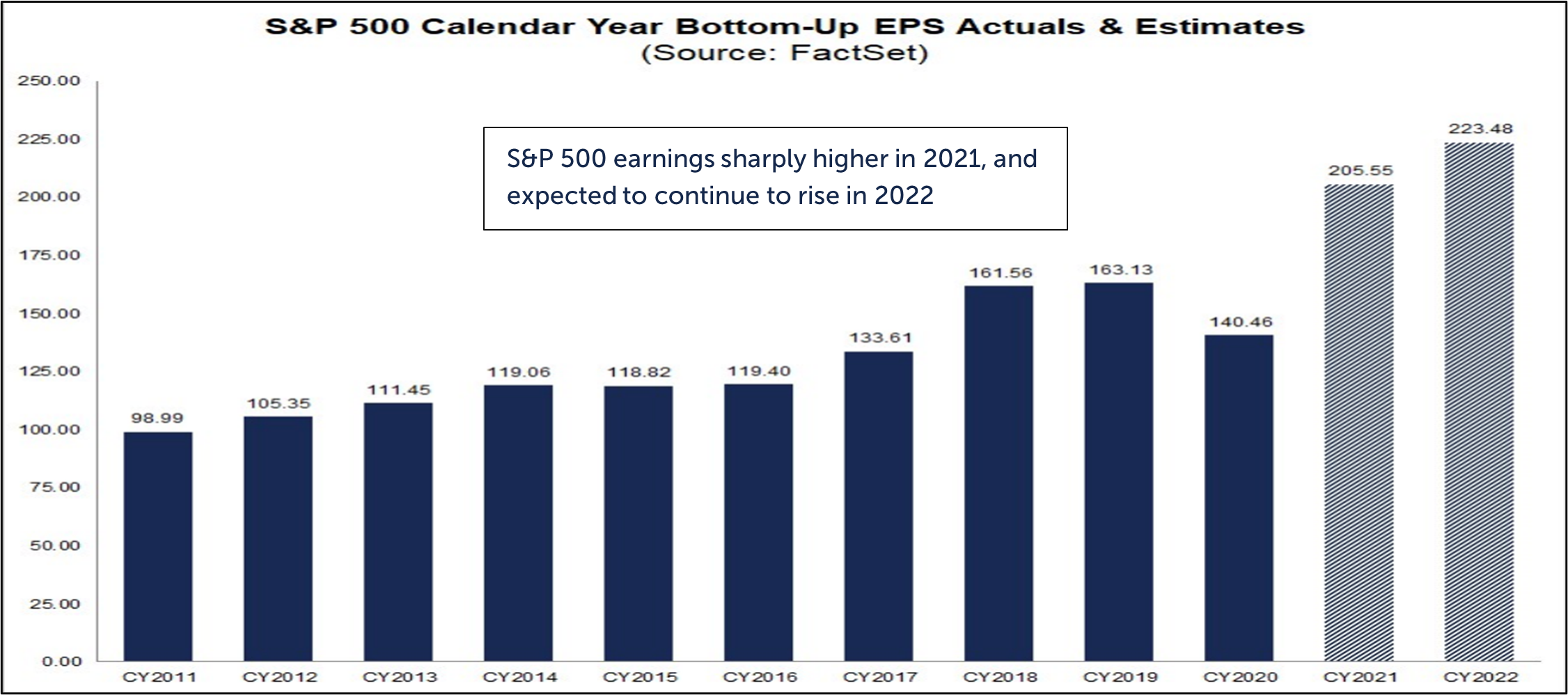

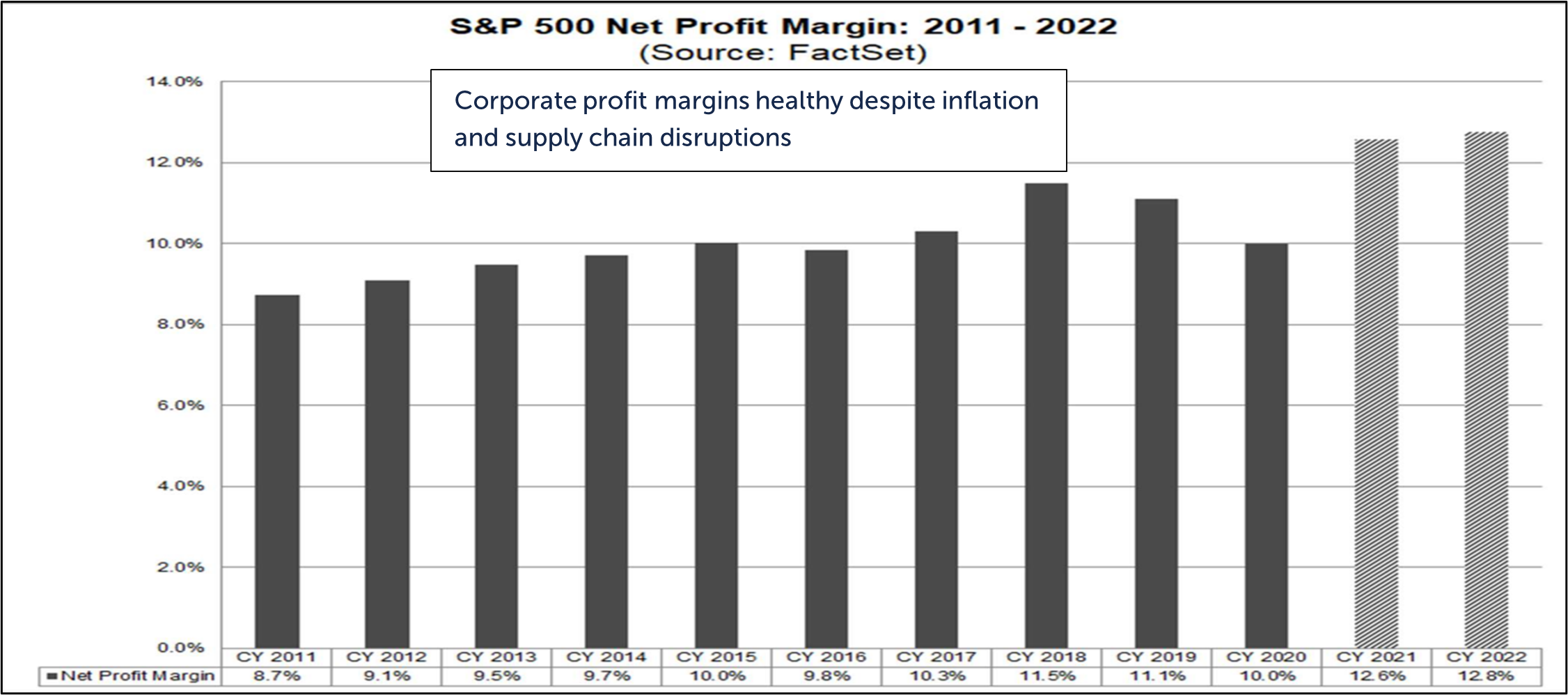

2021 was a robust year for corporate earnings growth. S&P 500 companies consistently outperformed analysts’ expectations all year, and future expectations for 2022 continued to be revised higher. At the start of the year, the index was barely expected to reach 2019 levels, the last full calendar year before the pandemic. However, S&P 500 earnings are expected to end the year more than 25% higher than 2019, and 2022 is expected to advance another 9%. Net profit margin, the amount investors earn after all business costs, debt service and taxes, also outperformed expectations in 2021. Along with earnings growth in 2022, it will be important for investors to monitor trends in company profitability to determine if they are able to manage higher costs for materials and labor.

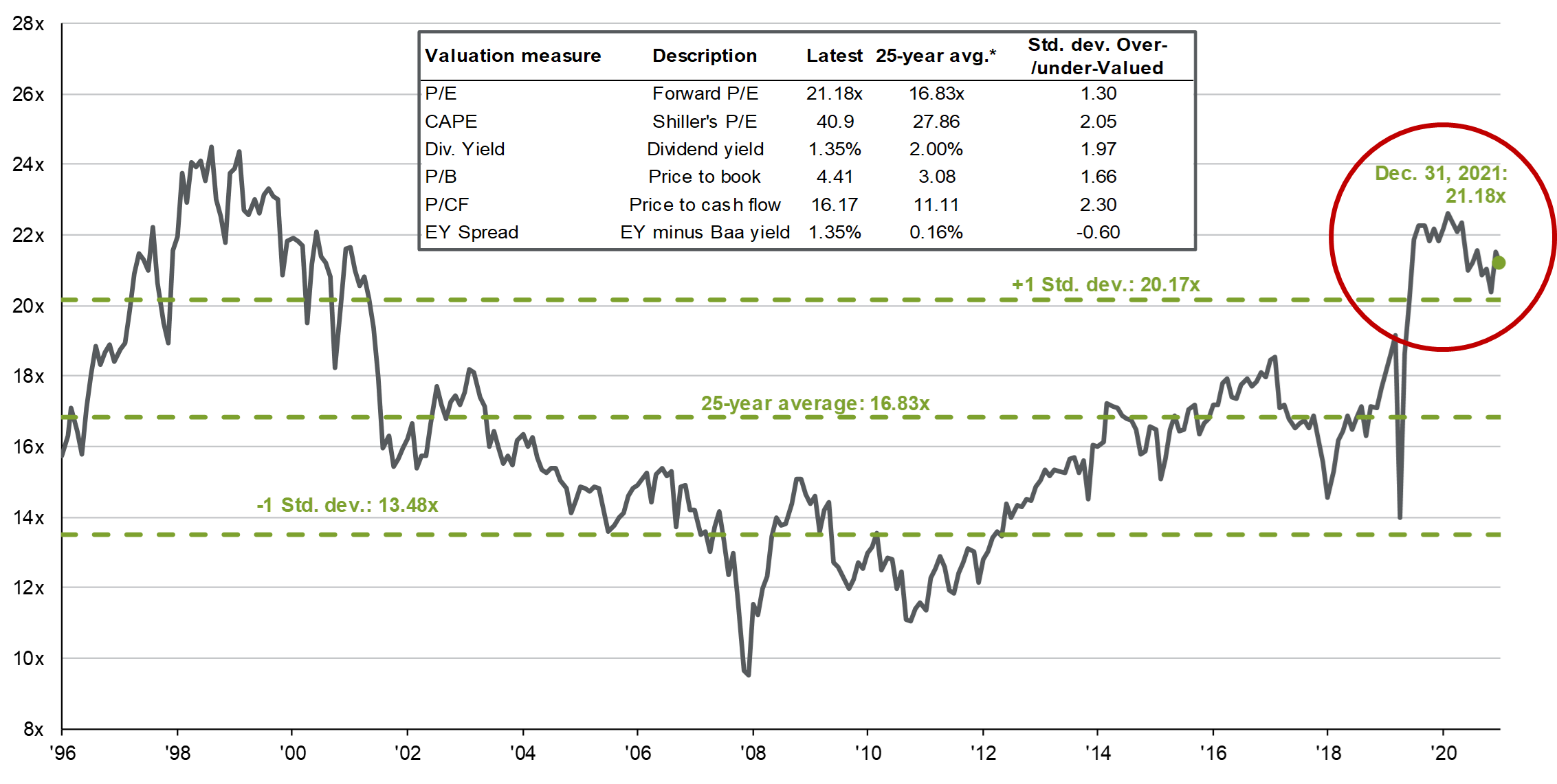

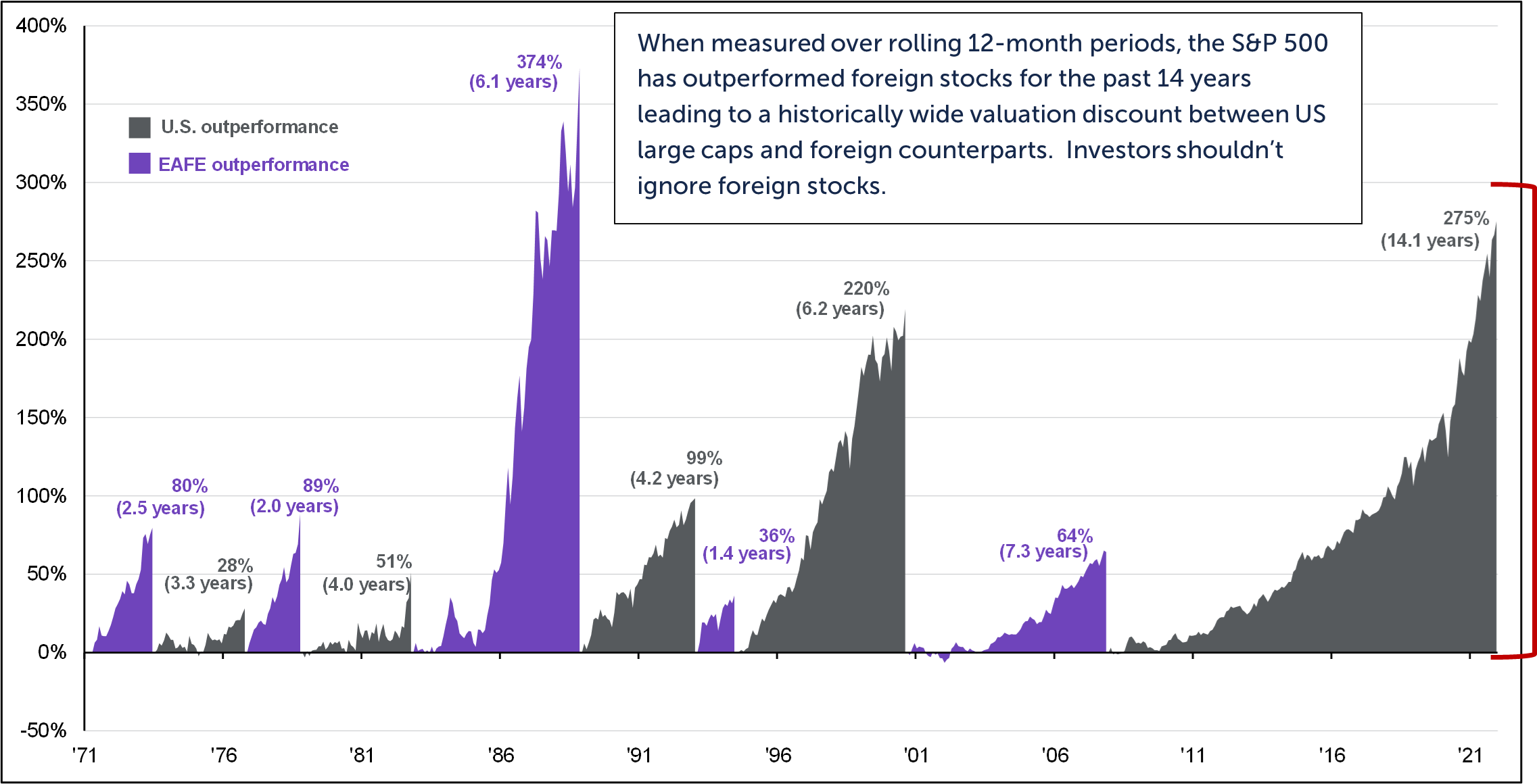

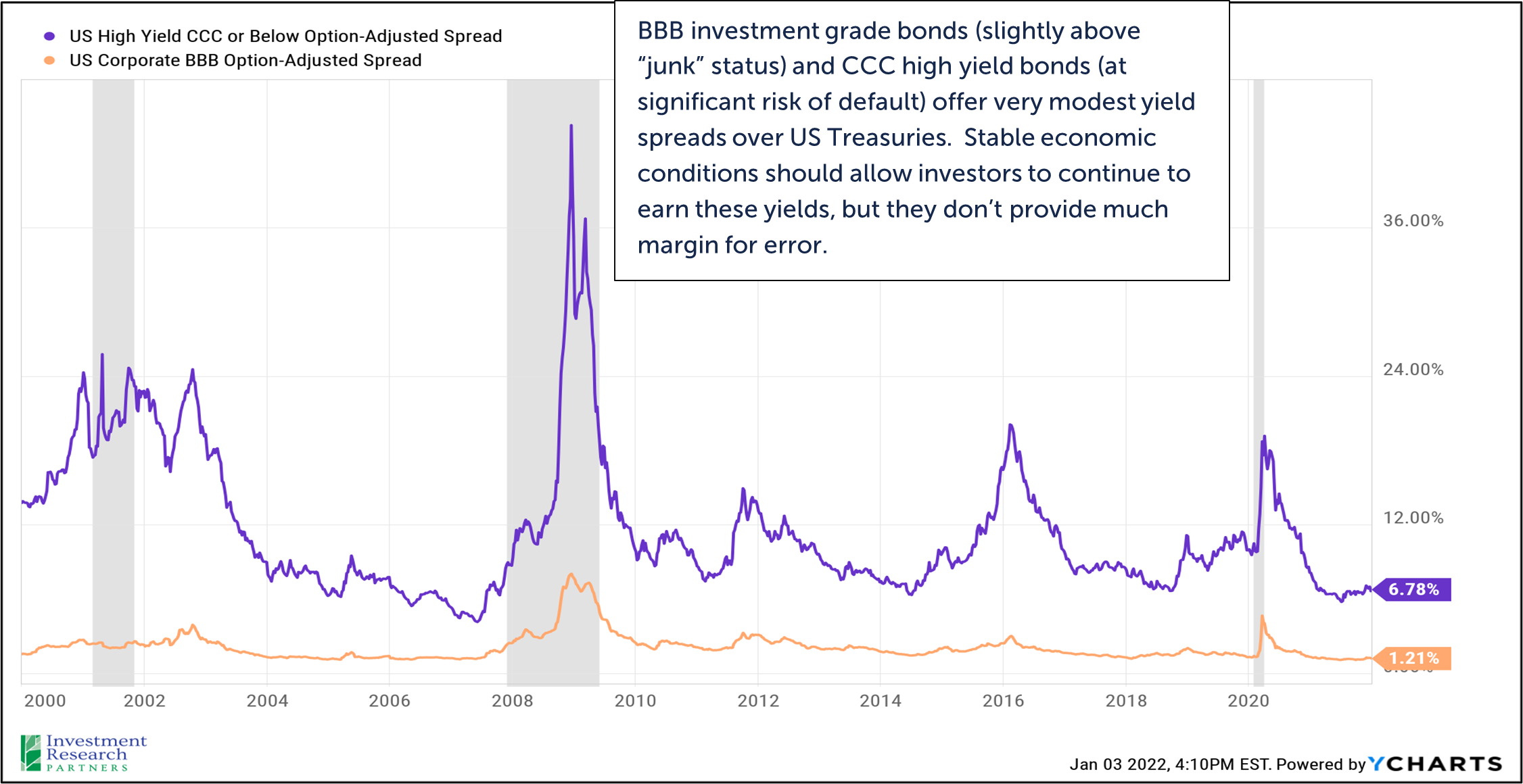

When assessing stock market valuation, investors often first look to the S&P 500 index as a gauge. When viewed on the aggregate index level, stocks do appear to be trading modestly rich relative to history. However, as highlighted by the valuation dispersion chart on page 4, the index-level data is not an accurate representation of today’s market. A historically high level of the S&P 500’s market cap is represented by just ten companies.[2] Foreign equities may offer relative value as these asset classes now trade at historically low discounts to their US counterparts. Lastly, US credit remains unattractive based on very modest yields relative to potential risks.

Source: FactSet, FRB, Robert Shiller, Refinitiv Datastream, Standard & Poor’s, Thomson Reuters, J.P. Morgan Asset Management as of December 31, 2021.

Prices & Interest Rates

| Representative Index | Current | Year-End 2020 |

|---|---|---|

| Crude Oil (US WTI) | $75.37 | $48.52 |

| Gold | $1,828 | $1,893 |

| US Dollar | 95.67 | 89.94 |

| 2 Year Treasury | 0.73% | 0.13% |

| 10 Year Treasury | 1.52% | 0.93% |

| 30 Year Treasury | 1.93% | 1.65% |

| Source: Morningstar, YCharts, and US Treasury as of December 31, 2021 |

Asset Class Returns

| Category | Representative Index | Full Year 2021 | Full Year 2020 |

|---|---|---|---|

| Global Equity | MSCI All-Country World | 18.5% | 16.3% |

| Global Equity | MSCI All-Country World ESG Leaders | 20.8% | 16.0% |

| US Large Cap Equity | S&P 500 | 28.7% | 18.4% |

| US Large Cap Equity | Dow Jones Industrial Average | 21.0% | 9.7% |

| US Large Cap Equity | Russell 3000 Growth | 25.9% | 38.3% |

| US Large Cap Equity | Russell 3000 Value | 25.4% | 2.9% |

| US Small Cap Equity | Russell 2000 | 14.8% | 20.0% |

| Foreign Developed Equity | MSCI EAFE | 11.3% | 7.8% |

| Emerging Market Equity | MSCI Emerging Markets | -2.5% | 18.3% |

| US Fixed Income | Bloomberg Barclays Municipal Bond | 1.5% | 5.2% |

| US Fixed Income | Bloomberg Barclays US Agg Bond | -1.5% | 7.5% |

| Global Fixed Income | Bloomberg Barclays Global Agg. Bond | -4.7% | 9.2% |

| Source: YCharts as of December 31, 2021 | |||

[1] Source: Bloomberg

[2] Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management as of December 31, 2021

Download PDF Version

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data. Please contact your Financial Advisor in order to complete an updated risk assessment to ensure that your investment allocation is appropriate.