April 1, 2021 •OneAscent

US stock market indices, such as the S&P 500, touched new all-time highs in March as economic, household, and business data all continued to imply that the recovery from the COVID-19 economic recession remains on track and stable. As of this writing, more than 167 million vaccine doses have been administered in the US, leading to the full vaccination of 62.4 million Americans (19% of the US population)[1]. In addition, the US federal government and Federal Reserve have pledged ongoing support to the economy in the form of low interest rates, abundant liquidity, and financial support for households and businesses.

Year-to-Date Index Performance (Hypothetical Growth of $100)

-OneAscent-Monthly-Investment-Update-April-2021.png)

Large Cap US Stocks represented by the S&P 500 index, US Growth Stocks represented by NASDAQ, Small Cap US Stocks represented by Russell 2000, Foreign Developed Market Stocks represented by MSCI EAFE, US Bonds represented by Bloomberg Barclays US Aggregate Bond

Source: Bloomberg

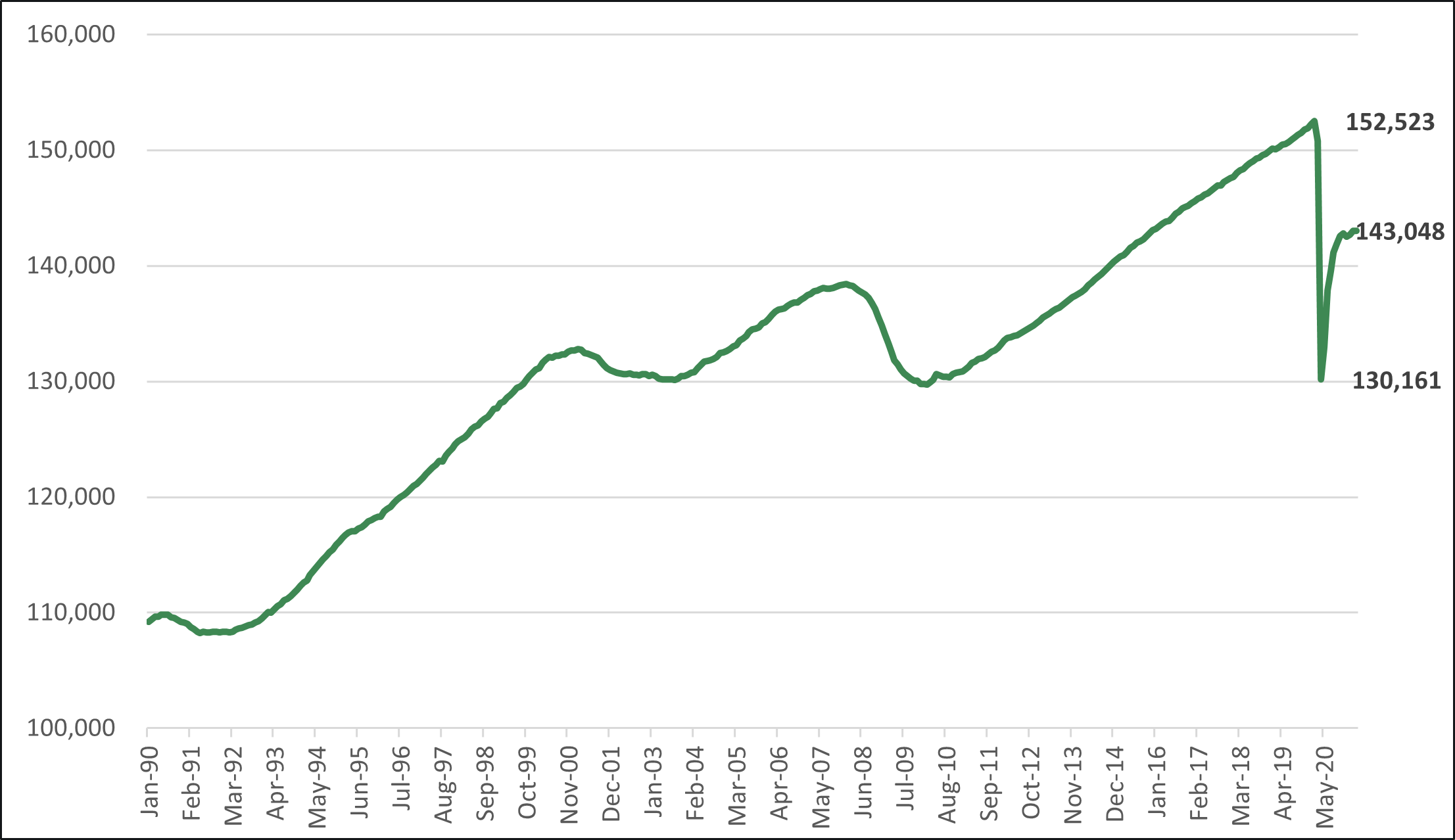

The labor market has continued its recovery, though the total number of employed Americans is still well-below pre-pandemic levels (see chart below). In early April, the US Bureau of Labor Statistics released their monthly assessment of labor market conditions. The unemployment rate declined to 6.0% as 916,000 new jobs were added to the economy. Of the new jobs added, the majority were in the leisure and hospitality industry (280,000), which is reasonable given the increase in restaurant, hotel, and travel activity witnessed as the vaccination program advances. Other notable sectors with job gains include construction (110,000) and manufacturing (53,000).[2]

Total Non-Farm US Payrolls (millions)

Source: Bloomberg

In March, Washington approved an additional $1.9 trillion stimulus bill in order to help blunt the impact of the COVID-19 virus on society, households, and businesses. Some key provisions within the bill include:

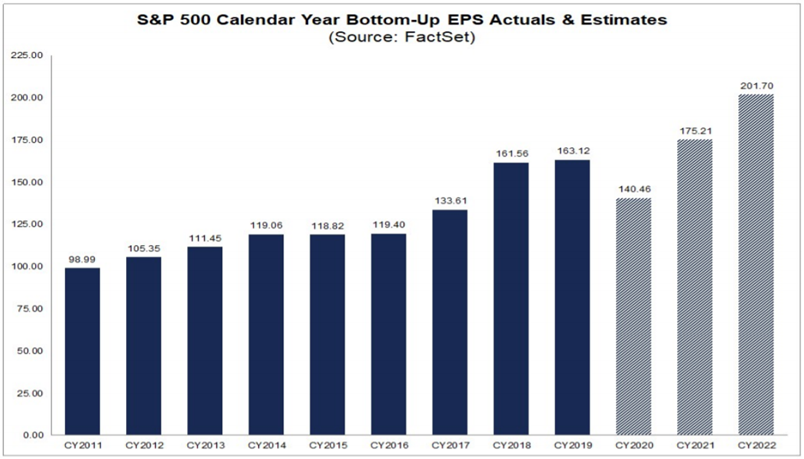

Expectations for Q1 earnings have been increasing with analysts now estimating year-over-year earnings growth for the S&P 500 index during the quarter to be 23% higher than last year, which is up from the 16% growth expectation at the end of December. For calendar year 2021 and 2022, the consensus analyst estimate is for the S&P 500 to earn $175 and $202, respectively. Given that the index is trading at approximately 4,000 as of this writing, this would imply that investors are willing to pay 23x for 2021 earnings and 20x for 2022 earnings. While these multiples are above long-term averages, the low interest rate environment and robust expectation for earnings growth may be supporting investors’ enthusiasm. It is important to note that these are only estimates for index earnings in 2021 and 2022, so investors may experience significant price compression in the index if these earnings gains fail to materialize.

The unique nature of this most recent recession, marked by a very sharp contraction in economic activity due to government mandated limits on activity followed by unprecedented fiscal and monetary stimulus as well as a quick economic reopening, may have potentially created some logistical challenges. In other words, factories and other key elements of the global supply chain may have shut down for economic or health-related reasons, and now must get back online quickly to support significant demand stemming from cash rich households and businesses. These significant gaps in supply juxtaposed against above-average demand are likely creating inflationary pressures. Investors would be wise to track the level and trend of headline inflation as well as its underlying components, and to consider portfolio hedges accordingly. A key question will be determining if these indications are short-lived and transitory or part of a longer-term cycle of higher prices, which could have broader implications on both fixed income and equities.

Asset Class Returns

| Category | Representative Index | March 2021 | YTD 2021 | Full Year 2020 |

|---|---|---|---|---|

| Global Equity | MSCI All-Country World | 2.7% | 4.6% | 16.3% |

| US Large Cap Equity | S&P 500 | 4.4% | 6.2% | 18.4% |

| US Small Cap Equity | Russell 2000 | 1.0% | 12.7% | 20.0% |

| Foreign Developed Equity | MSCI EAFE | 2.3% | 3.5% | 7.8% |

| Emerging Market Equity | MSCI Emerging Markets | -1.5% | 2.3% | 18.3% |

| US High Yield Fixed Income | ICE BofAML High Yield Bond | 0.2% | 0.9% | 6.2% |

| US Fixed Income | Bloomberg Barclays US Aggregate Bond | -1.3% | -3.4% | 7.5% |

| Cash Equivalents | ICE BofAML 0-3 Mo Deposit | 0.0% | 0.0% | 0.5% |

| Source: Morningstar (total returns shown gross of fees) As of March 31, 2021 |

Prices & Interest Rates

| Representative Index | March 31st 2021 | Year-End 2020 |

|---|---|---|

| S&P 500 | 3,973 | 3,756 |

| Dow Jones Industrial Avg. | 32,982 | 30,606 |

| NASDAQ | 13,247 | 12,888 |

| Crude Oil (US WTI) | $59.16 | $48.42 |

| Gold | $1,714 | $1,902 |

| US Dollar | 93.23 | 89.94 |

| 2 Year Treasury | 0.17% | 0.13% |

| 10 Year Treasury | 1.73% | 0.93% |

| 30 Year Treasury | 2.36% | 1.65% |

| Source: Bloomberg, US Treasury (total returns shown gross of fees) As of March 31, 2021 |

[1] https://www.npr.org/sections/health-shots/2021/01/28/960901166/how-is-the-covid-19-vaccination-campaign-going-in-your-state

[2] https://www.bls.gov/charts/employment-situation/employment-by-industry-monthly-changes.htm

[3] https://www.wsj.com/articles/whats-new-in-the-third-covid-19-stimulus-bill-11615285802?mod=hp_lead_pos5

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data. Please contact your Financial Advisor in order to complete an updated risk assessment to ensure that your investment allocation is appropriate.