April 28, 2022 •OneAscent

Equity markets are once again in correction territory (defined a decline of 10% or more) with some parts of the market, such as technology stocks, officially in a bear market (a decline of 20% or more). In addition, volatility has been elevated in 2022 with the CBOE S&P 500 Implied Volatility Index (VIX) exceeding a reading of 30 on three separate occasions so far this year.

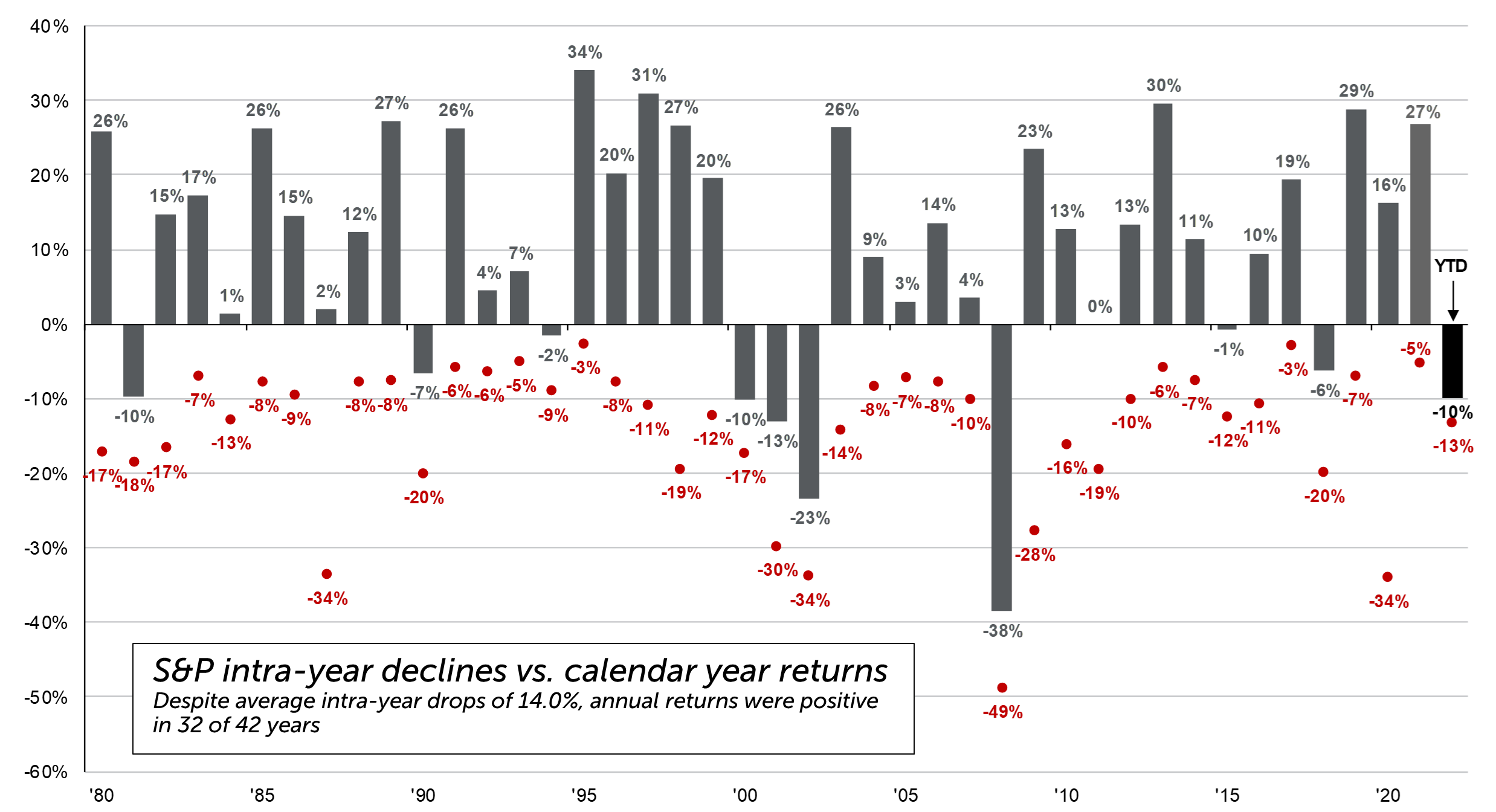

As of market close on April 26, the S&P 500 Index is down approximately 12% year-to-date 2022, in proximity to the lows reached in March. Although the volatility may be unnerving for some investors, we should note the pullback we have witnessed this year is nothing unusual compared to the roughly 14% average pullback markets have experienced over the last calendar 40 years.

Market corrections are often accompanied by economic or geopolitical uncertainties, and the year-to-date period is no exception. The major list of concerns includes the Russia-Ukraine conflict, the highest levels of inflation since the 1980’s, the Federal Reserve (Fed) raising interest rates, and continued supply chain effects from COVID (most recently in China). The most significant of these risks is the possibility of the Russia-Ukraine conflict spilling over into a global conflict and while we still view this outcome as unlikely, the recent ramping up of nuclear rhetoric is very concerning.

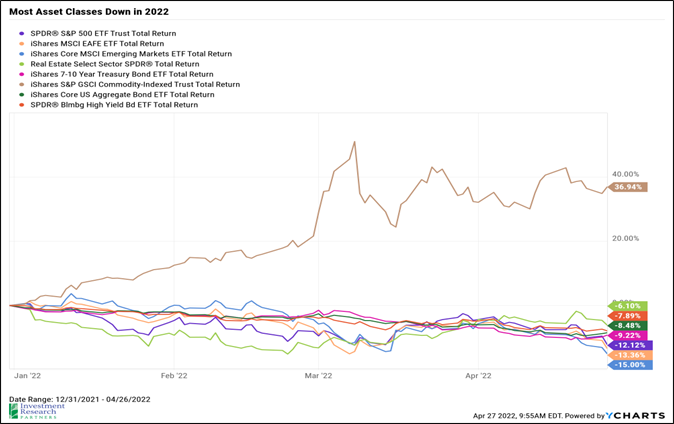

One of the unusual aspects of this correction, is that bonds have also fared poorly year-to-date. The Bloomberg Aggregate Bond Index down more than 8% over this period and have failed to provide offsetting positive returns.

As an investment committee, we discuss these risks as well as opportunities for the global markets and economy. We presently have a neutral outlook based on a balance of factors in the major categories we assess:

Inflation is negatively impacting consumer confidence and rising interest rates will slow important sectors like housing, construction and automotive. That said, leading economic indicators point to continued economic growth, the labor market is very strong, consumer finances are healthy, and corporate profits have held up well thus far.

Bond interest rates remain well below long term historical averages creating less opportunity for bond investors. In addition, overall S&P 500 valuation levels remain modestly above 25 year averages. However, valuation dispersions are high, creating lots of opportunity, especially in categories that remain undervalued or have declined significantly more than the broad-market year-to-date.

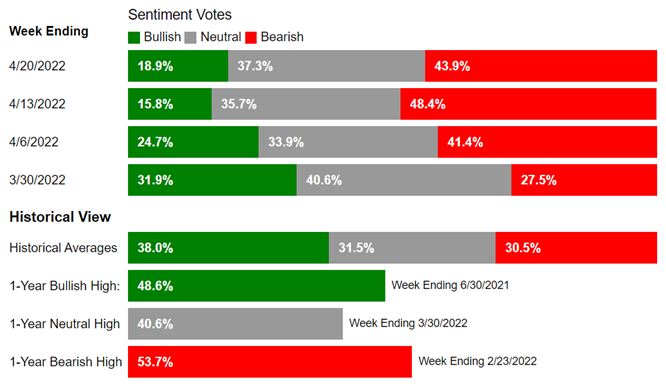

Market declines tend to be associated with a rotation out of equities and can change long term price trends. We have seen softening of market technicals year to date, but many parts of the equity markets remain above important long-term support levels. Retail investors have becoming increasingly bearish over the last month. The AAII weekly Investor Sentiment survey has had bullish readings below 20% for two consecutive weeks. When this has occurred in the past it has been associated with opportunistic buying times for long-term investors.

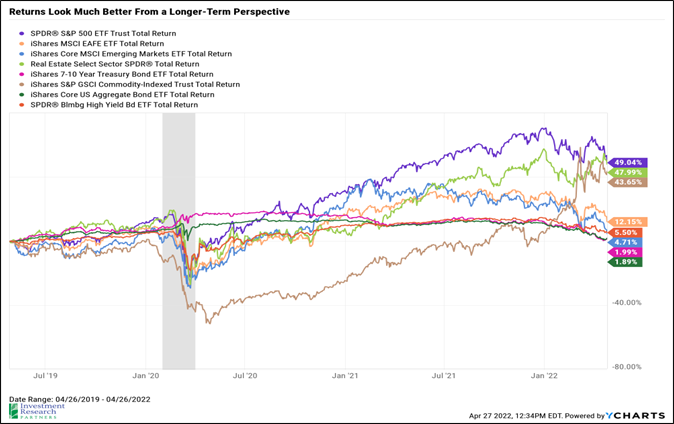

Investors seeking real growth of their wealth in the long-run likely recognize that volatility is a normal course of investing. 2021 was quite a calm year relative to most, and predictably, 2022’s market decline feels worse than average as a result, despite being right in-line with the average pullback. We continually seek long-term opportunities on your behalf, and welcome any discussion about your portfolio and goals.

|

Investors have turned very bearish in the last few weeks, often a contrarian signal.

Source: AAII

|

Download PDF Version

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data. Please contact your Financial Advisor in order to complete an updated risk assessment to ensure that your investment allocation is appropriate.