September 8, 2022 •Nathan Willis

Many wise investors hold to the stock market maxim, attributed to legendary investor Martin Zweig: “don’t fight the Fed.”[1] Investors would have done well to follow this advice in August as Jerome Powell, the Federal Reserve Chair, dominated the economic narrative and the movement of the markets.

Many wise investors hold to the stock market maxim, attributed to legendary investor Martin Zweig: “don’t fight the Fed.”[1] Investors would have done well to follow this advice in August as Jerome Powell, the Federal Reserve Chair, dominated the economic narrative and the movement of the markets.

After the roaring back from the June 16 lows – up 17% from June 16 at one point during August - the rally petered out, with the S&P 500 ending August up about 8% from those June lows.[2]

After the roaring back from the June 16 lows – up 17% from June 16 at one point during August - the rally petered out, with the S&P 500 ending August up about 8% from those June lows.[2]

The driver of these market moves was Fed Governor Powell’s 8-minute speech on the last Friday of August. Here are the highlights:

The Fed certainly faces a tough task, given its “dual mandate” of price stability and full employment. The Fed is raising rates alongside most central banks, illustrated in the chart below.

If the Fed can slow the economy to a goldilocks state – not too hot, not too cold – markets are likely to rebound. However, if the economy worsens from here, the stock market may take another leg down. As we have said several times recently, the key issue is whether or not things get worse from here, as the market is already pricing in a slowdown or even a mild recession.

Yogi Berra said, “If you don’t know where you’re going, you’ll end up someplace else.” The Fed knows exactly where it is going; we’ve been told that the destination is stable inflation – 2% is the Fed’s long-term target. The difficulty is what might need to happen on the journey there. The Fed is raising borrowing costs and getting ready to sell securities it owns – called quantitative tightening – after 10 years of quantitative easing that helped the stock market record exceptionally strong returns. This will create tighter financial conditions and slow the economy.

What does the Fed’s inflation fighting commitment mean for the markets?

Our Navigator process, focused on a data-driven review of Valuation, the Economy, Technical and Sentiment factors, can help us answer this question. Over the last couple of months, we have seen some changes.

Valuation: Valuation is neutral, as stocks and bonds have become cheaper this year – most stocks’ Price to Earnings ratios have gotten lower, and bond yields have increased. In fact, corporate bonds are more attractive now than they have been since the height of the pandemic.

Valuation: Valuation is neutral, as stocks and bonds have become cheaper this year – most stocks’ Price to Earnings ratios have gotten lower, and bond yields have increased. In fact, corporate bonds are more attractive now than they have been since the height of the pandemic.

Economy: The economy is a mixed bag with fear of an overaggressive Federal Reserve dominating the outlook. Employment is strong, and inflation may have already peaked, leading to uncertainty over the Fed’s committed course of action. We are watching earnings closely, as estimates for the third quarter of 2022 have begun to decline.

Technicals: Short-term technicals have indicated that, while choppy, the market still appears to be in a bottoming process. We are watching closely to confirm this while keeping track of evidence warning of further downside.

Technicals: Short-term technicals have indicated that, while choppy, the market still appears to be in a bottoming process. We are watching closely to confirm this while keeping track of evidence warning of further downside.

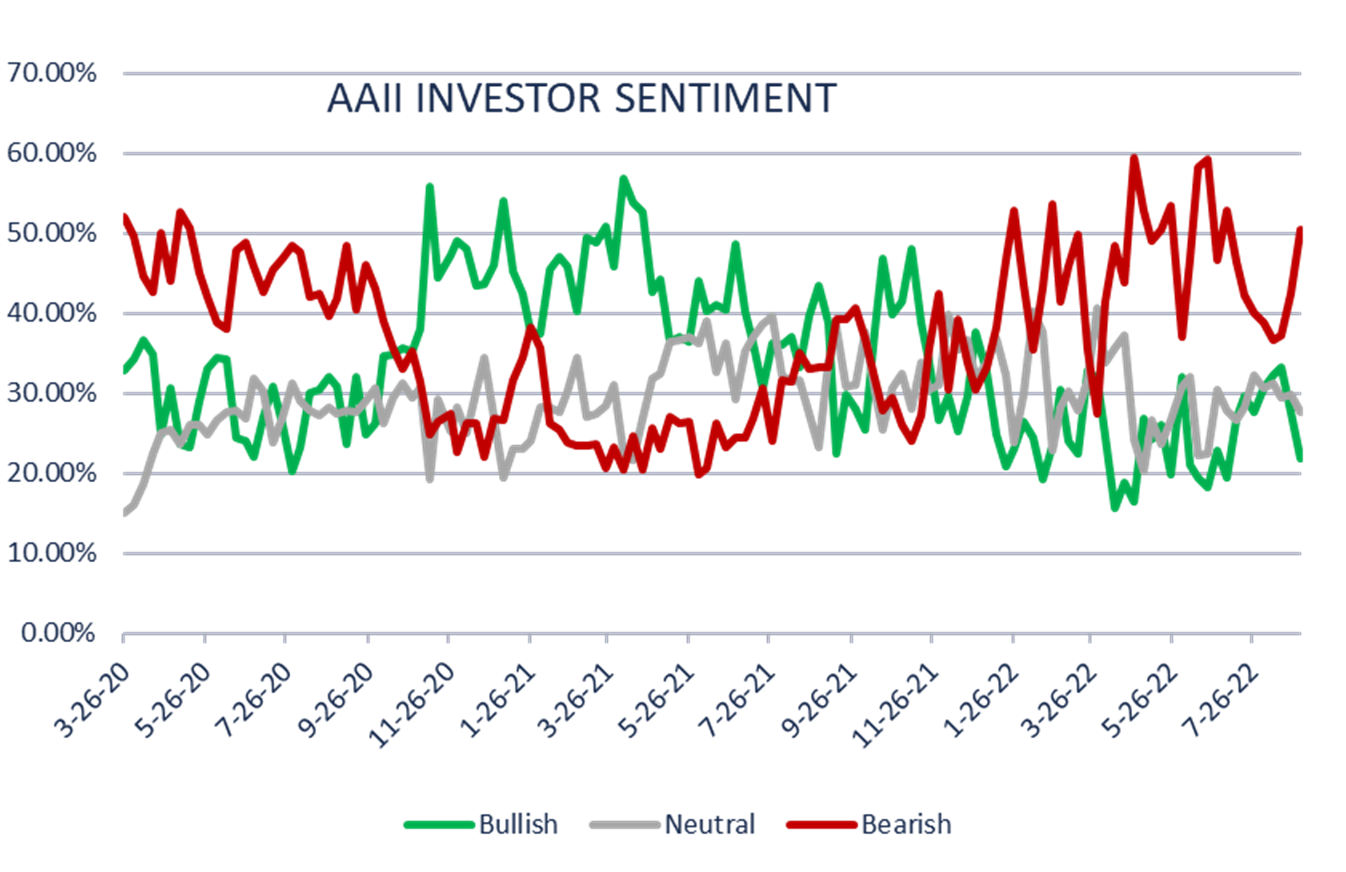

Sentiment: The American Association of Individual Investors survey is a well-known survey that we view as a contrarian indicator; when investors are negative on the stock market, that often means that the clouds contain silver linings. We see that situation today as the AAII survey bull minus bear measure has been negative for several weeks.[3]

In today’s environment, it pays to remember the quote at the beginning of this article: “Don’t fight the Fed.” They are committed to bringing down inflation. At the same time, we must maintain discipline.

We recommend investors take the following actions:

Even though the most balanced portfolios have lost a significant amount of money so far this year, returns are likely to be attractive over the coming months. And while the summer has finished with a lot of volatility in the stock market, we remind ourselves to stick with our plan, and we urge our partners to do the same.

[1] Martin Zweig, Winning on Wall Street, Warner books, 1986

[2] Source: Bloomberg

[3] Source: American Association of Individual Investors

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.